CCM Blockchain Newsletter (August 12, 2025)

Equities and bitcoin rallied last week, with bitcoin closing in on its July record high.

Happy Tuesday everyone, and welcome back to this week’s market newsletter. Please see below this week’s market data.

Bitcoin Market Update and News

- Bitcoin rebounds: Bitcoin dipped to as low as $113,000 last Tuesday before bouncing and finishing the week strong. At the time of publication, Bitcoin is up 5.6% week-over-week to $119,200.

- Trump signs executive order allowing for 401(k) allocation into Bitcoin: President Trump has paved the way for U.S. citizens to invest in crypto, real estate, private equity, and other assets with their 401(k)s. The executive order directs the Department of Labor to redefine qualified assets for 401(k)s to include spot cryptocurrencies and crypto ETFs. 401(k) portfolios account for an estimated $7.5 trillion.

Interesting Reads and Videos

- Breaking down Metaplanet’s play-by-play imitation of Strategy

- Ethiopia Intends to Wind Down Bitcoin Mining Citing Grid Strain

- The State of Bitcoin Adoption

Bitcoin Treasury Company News and Updates

- Strategy announces that it will no longer issue new MSTR shares below 2.5x mNAV, except to raise funds for dividends: Strategy indicated last week that it will no longer dilute its common stock, MSTR, when the stock is below a 2.5x multiple of net asset value (mNAV) — except for when it needs funds to pay out dividends on its four preferred shares, STRK, STRF, STRD, and STRC. These preferred shares pay annual dividends between 8-10% and are estimated to cost the company between $300-400 million annually.

- Strategy adds 21,021 BTC to treasury: Last week, Strategy announced that it purchased 21,021 BTC for $2.46 billion, increasing its total bitcoin holdings to 628,791 BTC valued at over $76.5 billion at the time of writing.

- 180 Life Sciences pivots to ETH treasury strategy, raises $425 million: Biotech firm 180 Life Sciences is rebranding as ETHZilla to launch an ethereum treasury strategy. The company disclosed that it has raised $425 million in a private placement, adding that it plans to avoid leverage to accumulate its ethereum treasury.

Market Overview

- Equities bounce back: Stocks surged last week as companies reported encouraging earnings growth for Q2. The Nasdaq hit a new all-time high, while the S&P 500 and Dow recouped the prior week’s losses, with the former just a hair away from its own record high.

- S&P 500: 6,389 (+2.4%)

- Nasdaq: 21,450 (+3.9%)

- Dow: 44,176 (+1.3%)

- Russell 2000: 2,218.42 (+2.4%)

- S&P 500 earnings continue to surpass expectations: According to FactSet, 90% of S&P 500 companies have reported Q2 earnings, and they continue to beat expectations. 81% of reported companies surpassed expectations, with the S&P 500’s blended average earnings growth increasing 11.8% year-over-year and revenue rising 6.3% quarter-over-quarter, the highest quarterly growth since Q3 2022 and above the 5.7% 10-year average. Given the results, FactSet reports that analysts have bumped expectations for earnings growth for Q2 from 3.8% to 9.7%, and they now forecast 7.2% growth in Q3, 7% in Q4, and 10.3% for 2025. The communications and technology sectors led earnings growth last quarter, while energy and materials were the only two sectors with negative earnings growth on average.

- Magnificent 7 leads Q2 earnings: The most valuable companies in the United States continue to significantly outperform the rest of the market. According to FactSet data cited by John Hancock, the Magnificent 7 is suspected to have a blended average growth rate of 25.7% YoY in Q2, versus 6.3% for the remainder of stocks in the S&P 500. Nvidia is the only company in the Magnificent 7 which has not reported their Q2 financials.

- Gold hits record high: Following a brief reprieve this summer, gold’s rally was reignited last week. Gold traded over $3,500 by the end of the week, but it sold off at the end of the week and into early trading hours on Monday to essentially negate the week’s gains. Year-to-date, gold is up 30%.

- Trump Administration rolls out tariffs on semiconductors as reciprocal tariffs take effect: New week, new tariffs. President Trump announced a 100% tariff on semiconductors. Companies that manufacture partly in the U.S. will be exempt. Additionally, the new reciprocal tariff schedule went into effect last Thursday. Most countries are facing 10-20% tariffs, although others face much higher rates. The U.S. is suspending tariffs on the European Union for six months as trade talks are ongoing, while Indian imports will face 50% tariffs starting August 27.

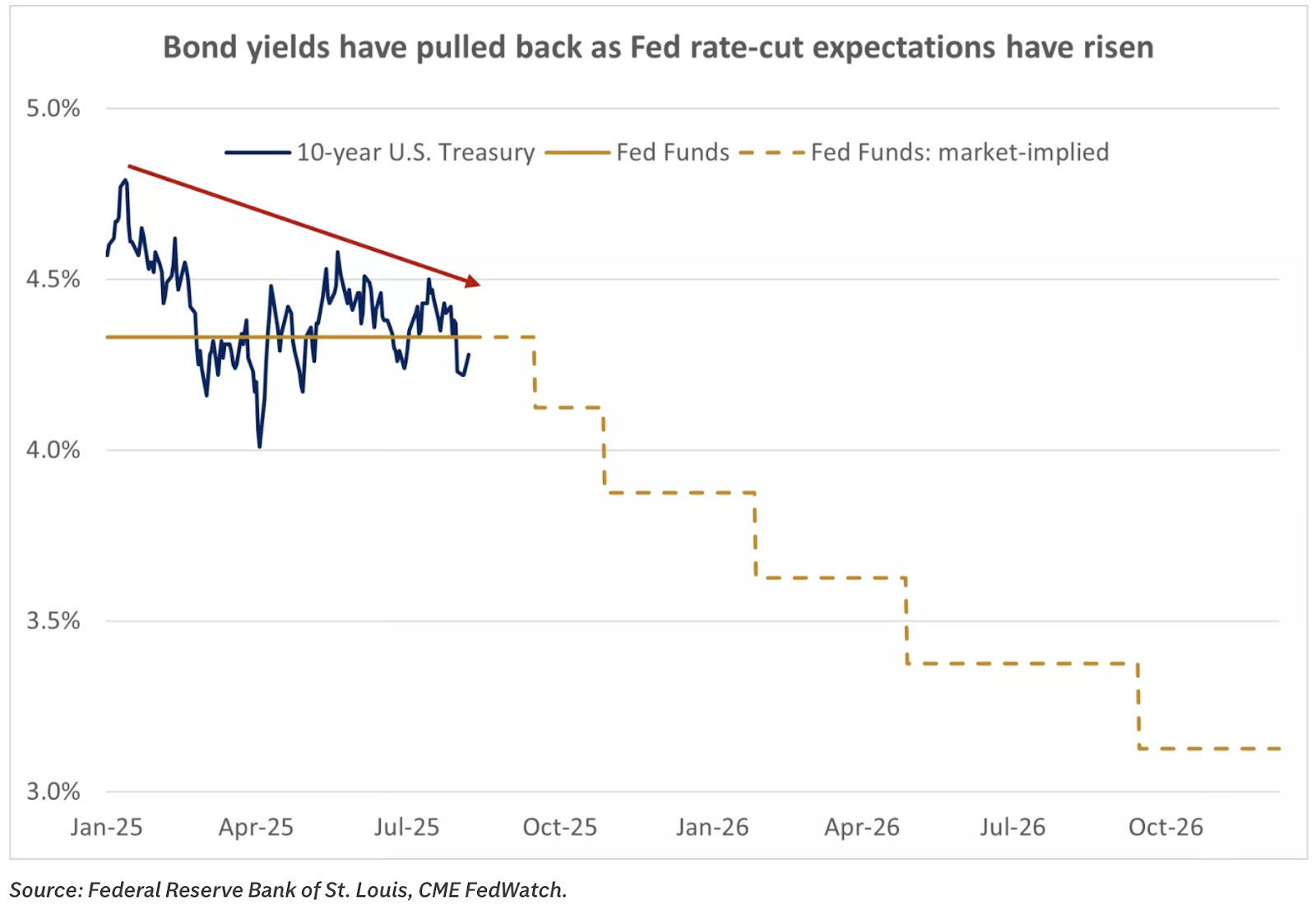

- Treasury yields rise: U.S. Treasury Bonds declined last week, pushing up yields as investors look for a safe haven for tariff uncertainty and as the U.S. Treasury auctioned $42 billion of 10-year and $25 billion of 30-year bonds last week.

- 30-Year: 4.85% (+0.03%)

- 10-Year: 4.28% (+0.06%)

- 5-Year: 3.82% (+0.06%)

- 2-Year: 3.76% (+0.08%)

- Oil takes a hit: Oil prices fell dramatically amid tariff jitters, fears of reduced demand, and OPEC+’s forecasted 547,000 barrels per day increase come September.

- WTI Crude: $63.88/bbl (-9.2%)

- Brent Crude: $66.59/bbl (-8.2%)

- S&P 500 Services Purchasing Managers Index hits 2025 high: The S&P 500 U.S. PMI increased to 55.7 in July, beating expectations for it to remain at 55.2 and above the 50 threshold which indicates expansion. The technology sector and financial services drove July’s increase. Companies reported a rise in output prices in response to tariff-induced increases to input costs.

- Consumer credit rises 2.3% in Q2: The Federal Reserve reported last week that total consumer credit rose 2.3% in Q2, driven by a 2.9% rise in non-revolving credit (versus 0.7% for revolving credit). In June alone, consumer credit grew 1.7%. Household credit grew $185 billion last quarter to $18.39 trillion, credit card balances rose $2 billion to $1.21 trillion, auto loans ticked up $13 billion to $1.66 trillion, and mortgage debt increased $131 billion to $12.94 trillion.

- Trade deficit shrinks in June: The U.S.’s goods and services trade deficit fell to $60.2 billion in June, down $11.5 billion (-15%) from May’s revised figure of $71.1 billion and the smallest deficit since September 2023. Exports totaled $277.3 billion (-0.5% MoM) and imports totaled $337.5 billion (-3.7% MoM), and the U.S. China Trade Deficit shrunk to $9.5 billion, the slimmest margin since 2004. Still, 2025’s cumulative deficit is 38.2% higher YoY (exports have averaged $282.2 billion, versus $346.2 billion for imports), largely driven by expedited imports to frontrun tariffs.

The week ahead in data:

- U.S. Bureau of Labor Statistics Consumer Price Index (Tuesday)

- U.S. Treasury federal budget (Tuesday)

- U.S. Bureau of Labor Statistics Producer Price Index (Thursday)

- U.S. Department of Labor weekly unemployment claims (Thursday)

- U.S. Census Bureau retail sales report (Friday)

- U.S. Census Bureau business inventories report (Friday)

- University of Michigan Index of Consumer Sentiment preliminary report (Friday)

- Federal Reserve industrial capacity and utilization (Friday)

- U.S. Bureau of Labor Statistics export and import prices report (Friday)

Notable corporate earnings this week:

- Archer Aviation (Monday)

- Barrick Mining (Monday)

- Franco‑Nevada (Monday)

- AMC Entertainment (Tuesday)

- CoreWeave (Tuesday)

- Circle (Tuesday)

- Cardinal Health (Tuesday)

- Sea Ltd. (Tuesday)

- Tencent Music (Tuesday)

- Cisco Systems (Wednesday)

- Applied Materials (Thursday)

- JD.com (Thursday)

- Deere & Company (Thursday)

- Flowers Foods (Friday)

Thank you for reading, and please feel free to reach out with any questions.