CCM Blockchain Newsletter (December 30, 2024)

Equities rose over the Christmas break, while bitcoin slumped.

Happy Monday, all, and welcome back to this week’s market newsletter. Please see below for this week’s market data, as well as a December update from Cohen & Company Capital Markets.

Market Overview

- Equities enjoy a holly jolly rally: Equities across the board experienced a holiday rally last week, bouncing back hard from the prior week’s general sell off. All the major indices closed in the green week-over-week; the Dow rose 1.65% to 42,992.21, the S&P 500 rose 2.21% to 5,970.84, the Nasdaq rose 2.77% to 19,722.03, and the Rusell 2000 rose 1.95% to 2,244.59.

- Oil rises, gas falls:

- Oil prices increased last week, with Brent Crude futures rising 1.9% week-over-week to $73.41/barrel by the end of Friday. The EIA expects U.S. oil production to increase by 300,000 barrels per day in 2025 for an average production of 13.7 million barrels per day, an increase that it forecasts will be concurrent with a global production boost of 1.6 million barrels per day. Given the expected growth in the U.S., the EIA also anticipates domestic imports to fall from 2.5 to 1.9 million barrels per day, the lowest since 1971.

- Henry Hub decreased significantly last week, falling 6% to $3.51/MMBtu. The EIA is expecting 2025 to be a record year for natural gas demand, and it likewise anticipates that U.S. exports will increase by a whopping 15% to 14 Bcf/day as the Plaquemines LNG and Corpus Christi LNG Stage 3 facilities come online for exports at the end of December. Further, the EIA expects U.S. natural gas production to average 103 Bcf/day in Q1 2025 and increase 1% for the full year, driven by increased production in the Permian and Eagle Ford regions.

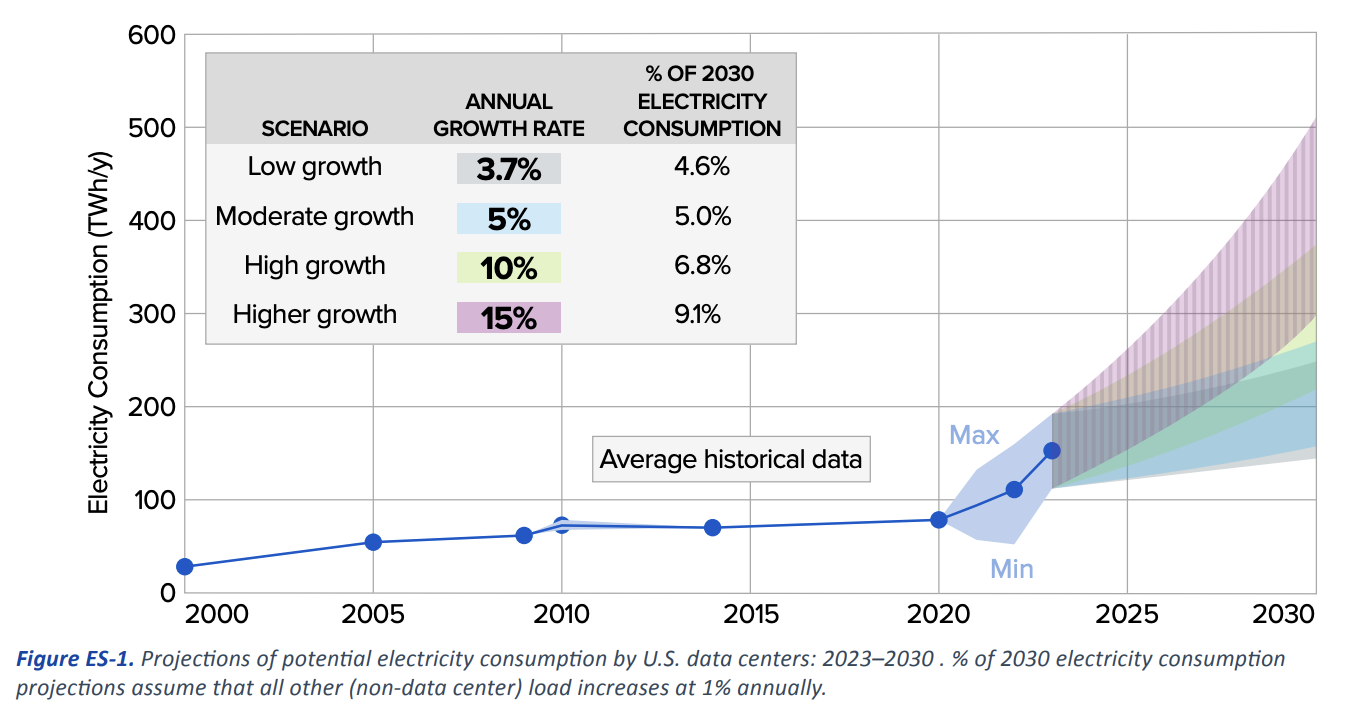

- Gas will be a key player in HPC/AI data center boom: Base load power plants like nuclear and natural gas will be indispensable for the coming wave of HPC and AI data centers in the United States. Per estimates from the Electric Power Research Institute (EPRI), U.S. data center electricity consumption could grow at a rate between 3.7-15% from 2023 to 2030.

- Treasuries rise despite Fed rate cut: Even as the Federal Reserve cut interest rates last week, U.S. Treasury yields rose across the board. The 10-year rose 10 bps to 4.62%, the 5-year 8 bps to 4.45%, and the 2-year 1 bp to 4.31%. Yields could be rising despite the cut for a number of reasons, including inflation expectations, the Fed’s forward guidance for slowed rate cuts in 2025, expectations of future fiscal stimulus, and other factors.

- Holiday goodies were 5% more expensive than last year: Christmas shoppers spent 5.4% more this year on their gifts than last year, with service-related gifts seeing the largest increase, according to JP Morgan. This coincided with an expectation-beating 0.7% increase to retail sales month-over-month.

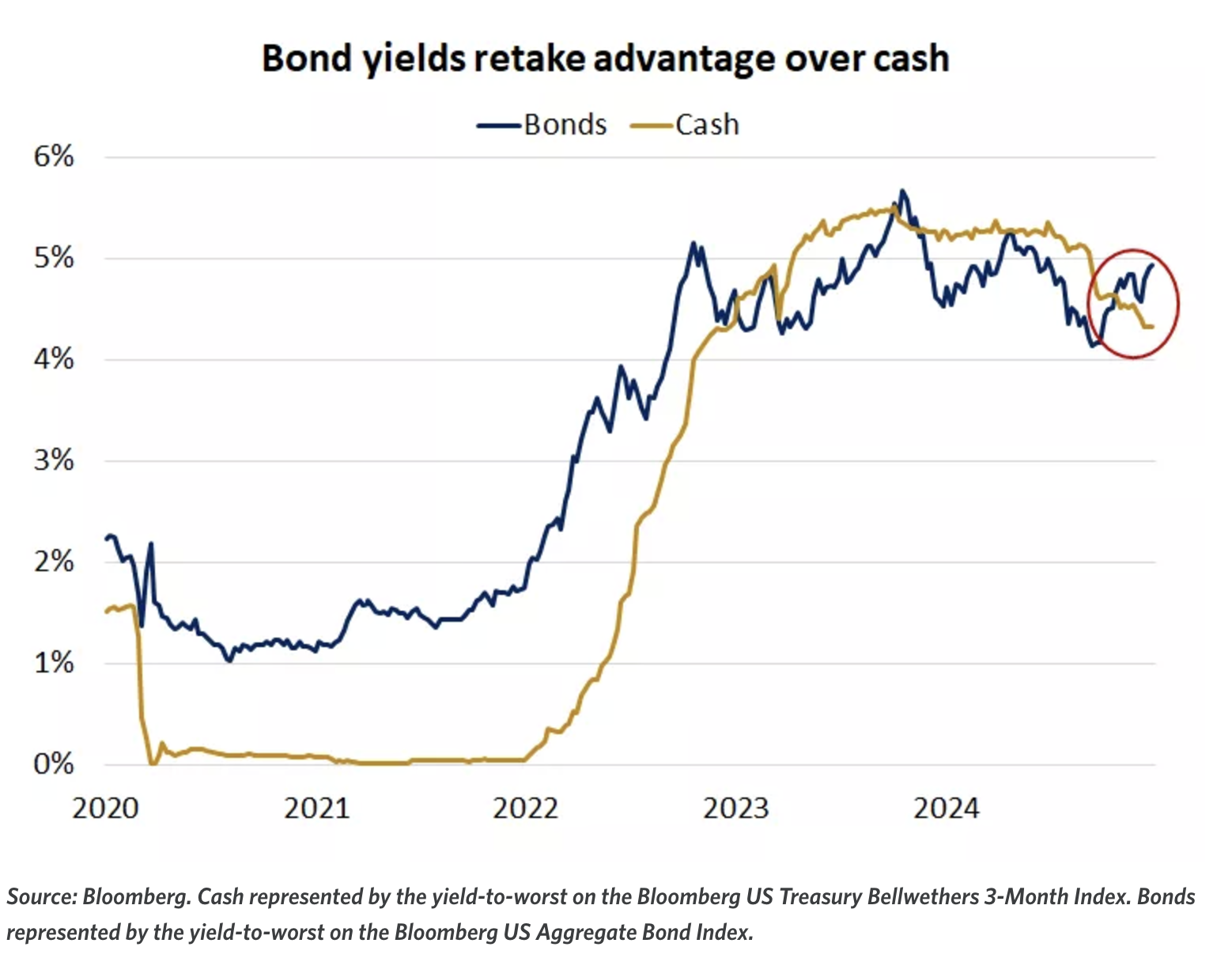

- Bond yields overtake cash: Following the Federal Reserve’s rate cuts two weeks ago, bond yields have overtaken cash yields. Per Edward Jones, investors extracted attractive yields from CDs, money market funds, and other cash instruments over the past few years after the Fed’s 2022 and 2023 rate hikes, but over the long term, bonds may provide greater yields (as Edward Jones points out, from 1981, U.S. investment-grade bonds averaged 6.8% returns to cash’s 4.1%).

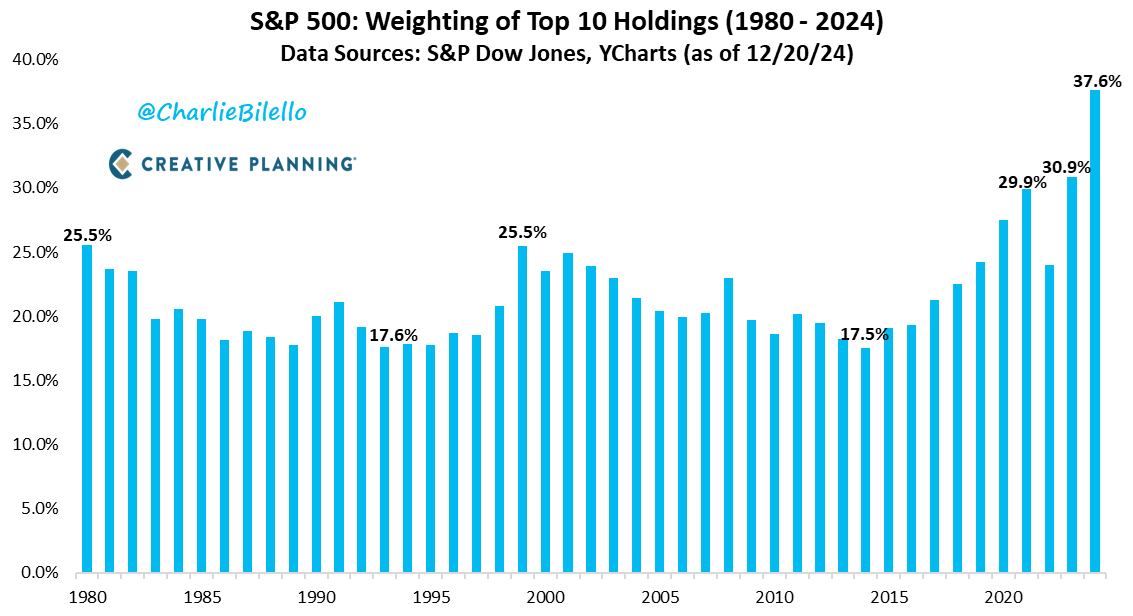

- S&P 500’s top holdings now constitute 37% of the index: The top 10 holdings in the S&P 500 now make up 37% of the index’s weighting.

The week ahead in data:

- National Association of Realtors November Pending Home Sales (Monday)

- Dallas Federal Reserve Bank December Manufacturing Survey (Monday)

- S&P Case-Shiller October Home Price Index (Wednesday)

- U.S. Census Bureau November Construction Spending report (Thursday)

- Labor Department unemployment claims (Thursday)

- S&P December Final U.S. Manufacturing PMI (Thursday)

- Institute for Supply Management December Manufacturing PMI (Friday)

Notable corporate earnings this week:

- Cal-Maine Foods (Monday)

- Lindsay Corporation (Thursday)

- Greenbrier Companies (Friday)

Bitcoin Market Update and News

- Bitcoin goes bah humbug over holidays: Bitcoin took a Christmas tumble last week, falling from $97,300 from December 20 to $94,200 at market close on December 27. At the time of publication, Bitcoin is trading at $92,600.

- Fold, Inc. Announces Up To $30 Million Convertible Note Financing Backed by Bitcoin: Today, Fold announced that it has closed a $20 million convertible note offering, using a portion of its bitcoin treasury as part of the collateral for the note. The note will mature in three years after Fold goes public, and the financial services company has the option to raise another $10 million under the offering.

- Exodus becomes first Bitcoin wallet provider to hit the big time: Exodus, one of the longest standing Bitcoin software companies, made its debut on a major public market two weeks ago. The company launched on the NYSE American on Wednesday, December 18, after trading for years on listed OTC markets.

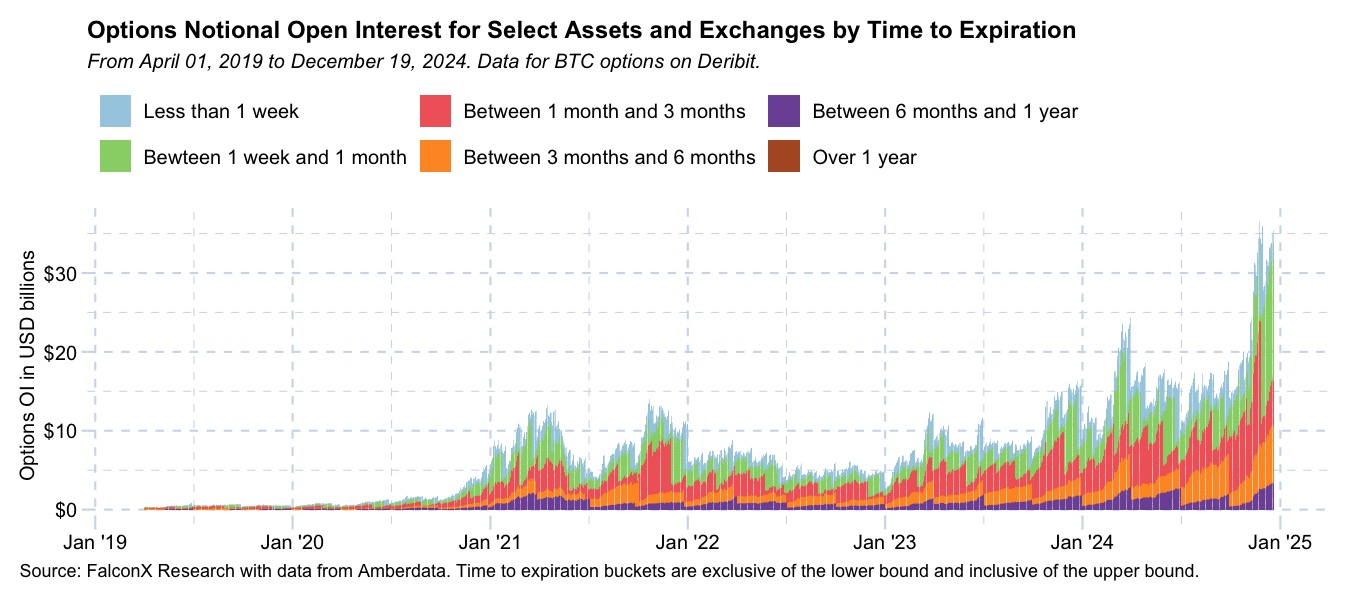

- December 27 saw Bitcoin’s biggest option expiry ever: Last Friday marked the biggest expiration of options in Bitcoin’s history. Per FalconX Head of Research David Lawant, “The December 27 expiry commands $15 billion in open interest and roughly $1 billion in daily volume. For context, these figures account for 43.0% and 35.8% of total market activity across all expiries and surpass the scale of the entire options market from just a few quarters ago… Looking at the strike-by-strike distribution, the six largest positions are in a mix of in-the-money and out-of-the-money calls: $90k, $100k, $110k, $120k, and $80k. Put activity clusters mainly around $80k and $90k strikes.”

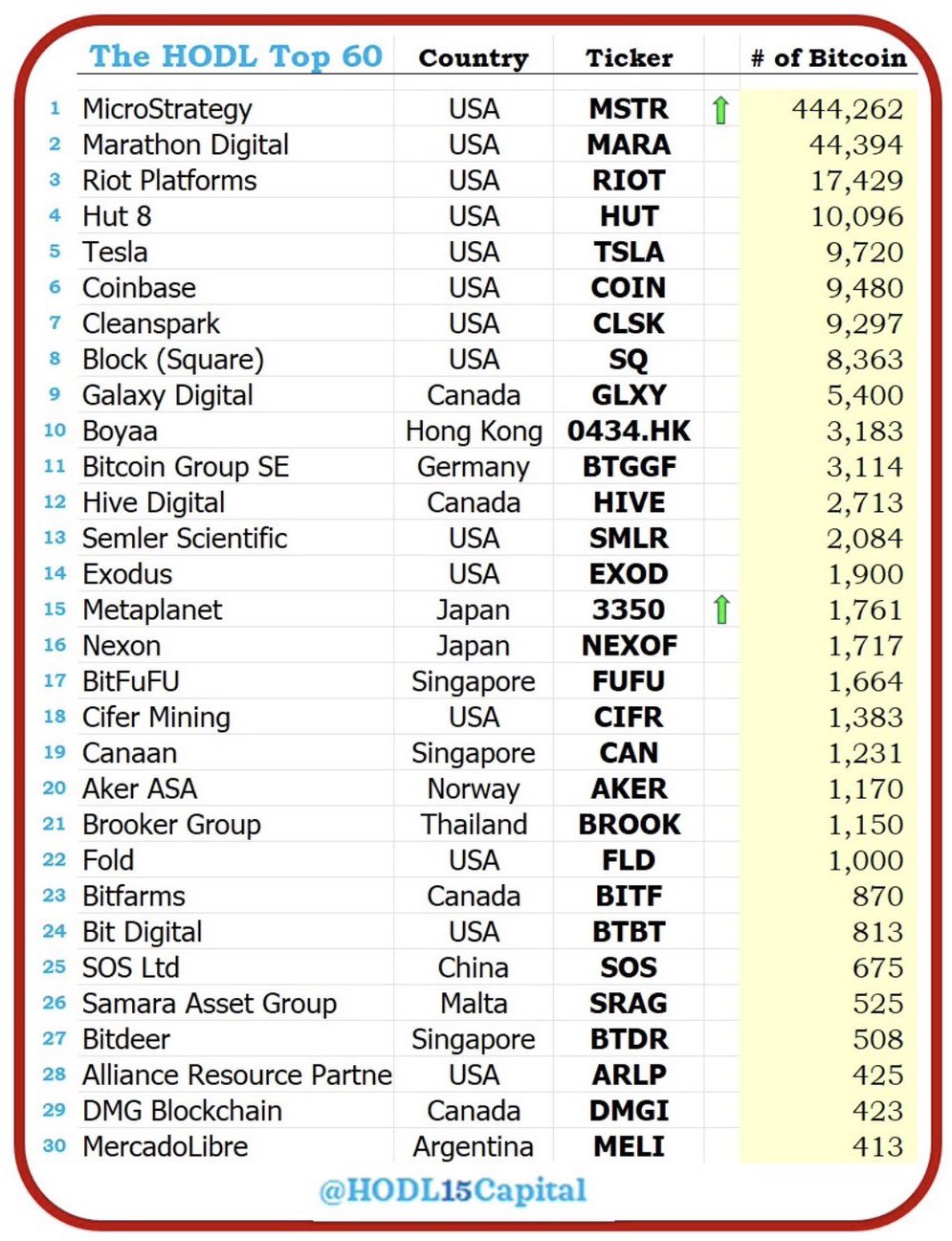

- Bitwise files for “Bitcoin Standard Corporation ETF”: Bitwise has a Bitcoin ETF with $4 billion AUM, but it’s not stopping there. The Bitcoin financial services firm filed for what it calls the Bitwise Bitcoin Standard Corporations ETF last week. If approved, this ETF would consist of a basket of publicly traded bitcoin companies that hold at least 1,000 BTC on their balance sheet, have a market capitalization of $100 million, and average $1 million in trading volume per day. There are currently 22 public (or soon-to-be public) companies that meet the 1,000 BTC threshold.

Interesting Reads and Videos

- What to watch in 2025: Africa making a mint from crypto mining boom

- Foundry Refunds 8.18 BTC in ‘Inadvertent’ Bitcoin Transaction Fees

- Russia is using bitcoin in foreign trade, finance minister says

Bitcoin Mining Market News and Trends

- Russian mining restrictions could be a boon to U.S. miners: Reports surfaced last week that Russian provinces are placing a moratorium on Bitcoin mining in the face of energy shortages; the bans will reportedly take place on January 1, 2025 and could last until March 15, 2031. While it won’t have nearly the same impact as China’s sweeping Bitcoin mining ban in 2021, it could still affect hashrate in one of the largest mining regions in the world, leaving miners in the U.S. and elsewhere to benefit from a potential downward difficulty adjustment and hashrate relocation.

- Bitdeer files for $1 billion shelf offering: Bitdeer, one of the largest publicly traded bitcoin miners by market cap and hashrate under management, has filed for a $1 billion shelf offering. With the offering, the company said it may sell shares, warrants, and/or debt securities. In addition to mining, Bitdeer has a burgeoning ASIC miner manufacturing business line, and it is also breaking into the AI/HPC computing field.

Thank you for reading, please feel free to reach out with any questions – and Happy New Year!

Christian Lopez