CCM Blockchain Newsletter (February 18, 2025)

Coinbase smashes earnings expectations, and Abu Dhabi piles nearly half a billion into bitcoin ETFs.

Happy Tuesday, all, and welcome back to this week’s market newsletter. Please see below this week’s market data.

Bitcoin Market Update and News

- Bitcoin mostly flat on the week: Bitcoin chopped sideways last week, bouncing between $96,000 and $98,000. At the time of publication, bitcoin is trading at ~$95,000.

- Coinbase delivers strong full-year earnings, beats expectations: Coinbase stock rose to a two-month high of $308 last Thursday after beating earnings expectations. The U.S.’s leading crypto exchange netted $2.27 billion in revenue in Q4 (versus an expected $1.84 billion), earning $4.68 per share (versus an expected $2.11). Coinbase’s total revenue was $6.6 billion for 2024 with $3.3 billion in adjusted EBITDA. Other KPIs for Coinbase’s 2024 earnings:

- $404 billion assets on platform

- 8.4 million monthly transacting users

- $1.16 trillion trading volume

- Consumer trading volume: $221 billion

- Institutional trading volume: $941 billion

- Consumer (retail) transaction revenue: $3.43 billion

- Institutional transaction revenue: $345.6 million

- Abu Dhabi sovereign wealth fund holds $461 million in bitcoin ETFs: Mubadala Investment Company, Abu Dhabi’s sovereign wealth fund, purchased $461 million of Blackrock’s IBIT bitcoin ETF in Q4. The stake makes it the seventh largest holder of IBIT.

Interesting Reads and Videos

- With Trump all-in on crypto, bitcoin bulls bet the trillions in cash on America's corporate balance sheets are next

- US-Designed Bitcoin Miner Delivers Promising Results

- Bitcoin mining industry created over 31K jobs in the US: Report

Bitcoin Mining Market News and Trends

- CBP seizes Antminers at ports of entry, expands detainment to MicroBT, Canaan ASICs: The U.S. Customs and Border Protection agency is expanding the reach of a crackdown on ASIC miner imports it started last fall. For the first time since the agency started detaining ASIC miners at ports of entry, it has now seized Antminer shipments from a number of North American bitcoin mining companies. It has also started detaining MicroBT and Canaan ASIC miners, whereas previous import holds were only affecting Antminer S21 and T21 models.

- IREN releases Q4 earnings, beats expectations: IREN released its Q4-2024 (Australian FY Q2-2025) earnings last week and outperformed analyst expectations. The company reported record revenue of $119.6 million and an adjusted EBITDA of $62.6 million. The company has 510 MW under management and a fleet efficiency of 15 J/TH, making it the best in the business currently. Even so, IREN spent much of its earnings call touting plans for its HPC/AI business line (which netted it $2.7 million in Q4), stating that it plans to carve out 75 MW on its Childress, TX site for AI/HPC computing load and that it is in the beginning stages of a 600 MW, second phase for its Sweetwater campus. The two Sweetwater sites would add 2 GW of power to IREN’s portfolio, and the company said that it is prioritizing a single AI/HPC tenant for these sites.

Market Overview

- Stocks rally, close near all-time highs: The big three indices rose last week, recovering from the losses they incurred the week prior. The S&P and Nasdaq closed just a hair shy of their all-time highs.

- S&P 500: 6,114.63 (+1.13%)

- Dow: 44,546.08 (+0.34%)

- Nasdaq: 20,026.77 (+1.82%)

- Russell 2000: 2,279.98 (-0.41%)

- Oil continues to slide while natural gas rises:

- U.S. oil prices fell for the fourth week in a row last week. WTI Crude closed at $70.74/barrel, a 0.67% decline.

- As of the EIA’s Wednesday update, Henry Hub rose 22% to $3.94/MMBtu. In its most recent Short-Term Energy Outlook, the EIA reported that the Henry Hub spot price averaged $4.13/MMBtu in January 2025, and it projects an average price of $3.80/MMBtu for 2025.

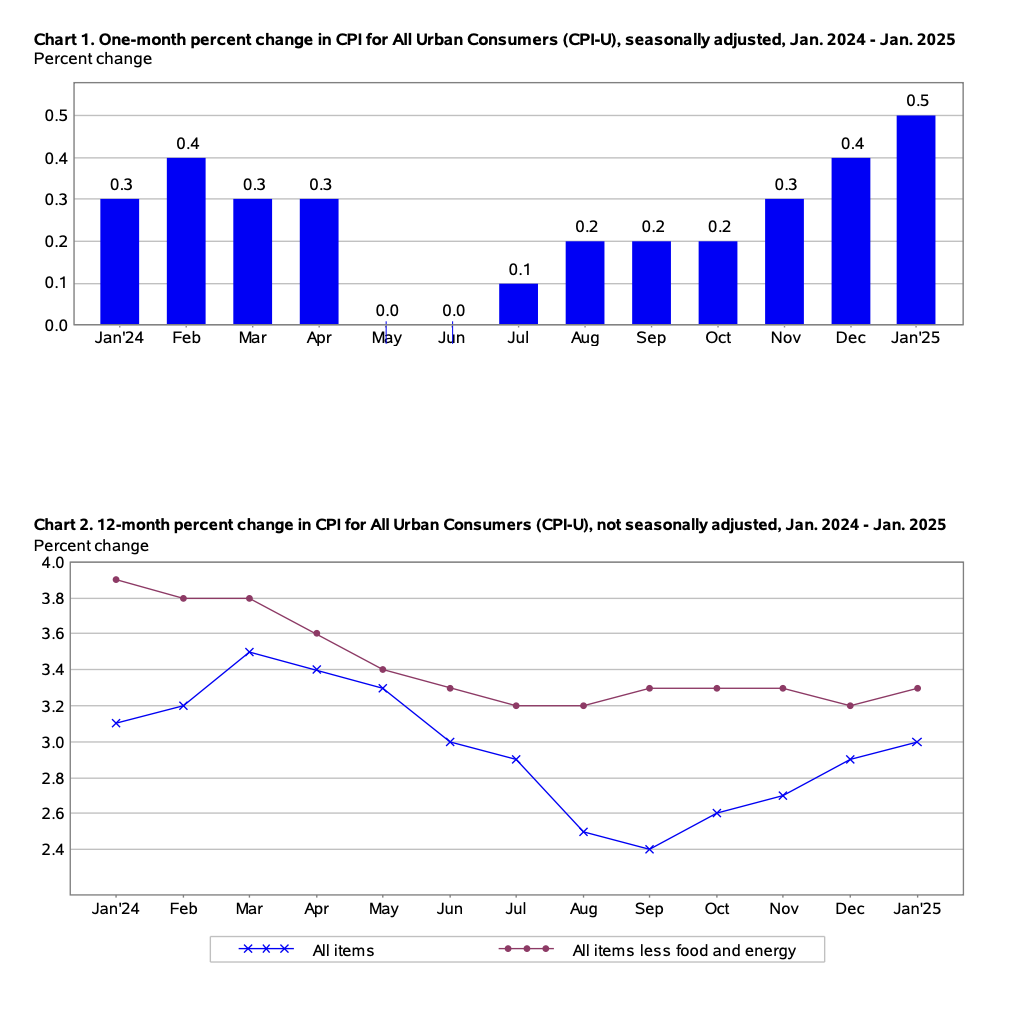

- With inflation sticky, Fed keeps rates steady: The CPI print for January came in hot last week. Core CPI increased by 3.3% annually while Headline CPI increased by 3% annually and 0.5% from December, the largest month-over-month change since August 2023. Meanwhile, retail sales for January were down 0.9%, according to the U.S. Census Bureau. With inflation still above the Fed’s 2% target, Jerome Powell reiterated in a congressional hearing last week that the Fed will need to see lower inflation before dropping rates.

- Treasury yields fall to cap off volatile week: Treasury yields bounced around last week, surging briefly on the inflation news only to close lower to end the week. The 10-year briefly hit 4.66%, but it closed the week down 2 bps to 4.48%; the 5-year closed down 1 bp to 4.33%; and the the 2-year closed down 2 bps to 4.26%.

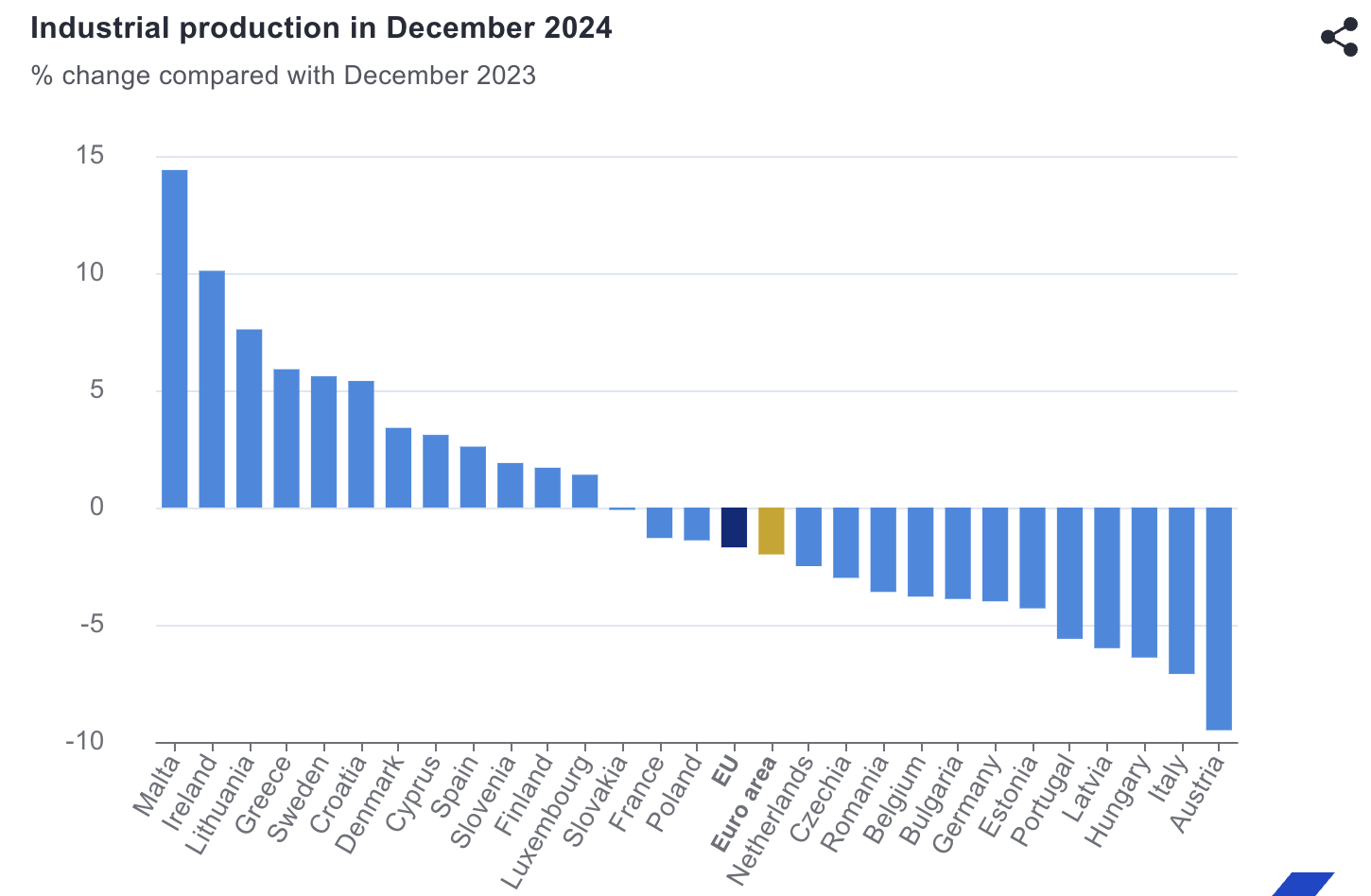

- European industrial production fell in December: Manufacturing capacity in the Eurozone and EU declined more than estimates in December. Month-over-month, industrial production fell 1.1% and 0.8% in the Eurozone and EU, respectively, and 2% and 1.7% year-over-year. The largest annual decreases came from Austria (-9.5%), Italy (-7.1%), and Hungary (-6.4%), while Germany’s production fell 4% year-over-year. The annual declines were largely driven by reduced production of capital goods (-8.1%), intermediate goods (-2.4%), and durable consumer goods (-2.2%).

The week ahead in data

- National Association of Home Builders Housing Market Index (Tuesday)

- U.S. Census Bureau housing starts report (Wednesday)

- FOMC meeting transcript release (Wednesday)

- Conference Board U.S. Leading Economic Index (Thursday)

- U.S. Department of Labor weekly unemployment claims (Thursday)

- University of Michigan Index of Consumer Sentiment final result (Friday)

- National Association of Realtors existing homes sales report (Friday)

Notable corporate earnings this week

- BHP (Tuesday)

- Arista Networks (Tuesday)

- Devon Energy (Tuesday)

- Occidental Petroleum (Tuesday)

- HSBC (Wednesday)

- Garmin (Wednesday)

- Baidu (Wednesday)

- Etsy (Wednesday)

- Analog Devices (Wednesday)

- Walmart (Thursday)

- Alibaba (Thursday)

- Newmont (Thursday)

- Block (Thursday)

- Rivian (Thursday)

Thank you for reading, and please feel free to reach out with any questions.

Christian Lopez