CCM Blockchain Newsletter (February 24, 2025)

Bitcoin sells off to low $90,000s, and the Magnificent 7 has some catching up to do.

Happy Tuesday, all, and welcome back to this week’s market newsletter. Please see below this week’s market data.

Bitcoin Market Update and News

- Bitcoin range bound last week, tumbles to start this week: Bitcoin was essentially flat last week despite almost making a break back above $100,000. But it has tumbled 4% today, and at the time of publication, bitcoin is trading at ~$91,000.

- Bitcoin financial services platform Fold goes public: Fold, a bitcoin financial services app that allows users to earn bitcoin rewards, made its public debut last week following its merger with FTAC Emerald Acquisition Corp. Fold’s core products include a bitcoin debit card that gives users BTC rewards on every purchase and an FDIC bank account that users can use to earn BTC when paying their mortgage, rent, and other expenditures. Fold projected $24 million in 2024 revenue according to an S4 filing, and it pulled in $21.5 million in 2023 and $28.9 million in 2022. Fold also has 1,000 BTC on its balance sheet, giving it both a financial cushion for development and a potential draw to investors looking for high beta exposure to bitcoin.

- GameStop is mulling over a bitcoin reserve: Two weeks ago, CNBC reported that GameStop is reportedly looking to park some of its $4.6 billion in cash in bitcoin. The gaming company was all but irrelevant to investors until the infamous retail-driven short squeeze in early 2021 that sent the stock to an all-time high of $483. CEO Ryan Cohen posted a photo with Strategy CEO Michael Saylor in early February, fueling speculation. If GameStop were to invest in bitcoin, it would perhaps be the biggest household name to adopt a bitcoin treasury strategy and could serve as a bellwether for the strategy’s evolution outside of Bitcoin and Bitcoin-adjacent companies.

Interesting Reads and Videos

- 1,500+ institutions have exposure to bitcoin

- Unpacking institutional allocations of bitcoin mining equities

- The Bitcoin Ecosystem – 2024 Annual Report

Bitcoin Mining Market News and Trends

- Core Scientific leases Alabama HPC data center, signals intent to purchase: Core Scientific has expanded its HPC footprint by leasing a data center in Alabama for 16 MW of high performance compute (HPC). The company announced that it may exercise an option to purchase the center for $135 million with approximately $400 million of additional capital expenditures to expand the campus. This acquisition strategy is a notable departure from Core Scientific’s current project to retrofit its existing bitcoin mines for AI/HPC computing load under a multiple billion dollar deal with CoreWeave. Core Scientific’s latest investor presentation forecasted that it should complete construction on the first 200 MW of this deal by the end of Q2 2025.

- New study shows job creation, multi-billion dollar impact of bitcoin mining on U.S. economy: A study conducted by the Perryman Group and commissioned by the Texas Blockchain Council and the Digital Chamber elucidates the economic impact of bitcoin mining on the Texas economy and the U.S. economy more broadly. In Texas, the report estimates that bitcoin mining has created $4.23 billion in total expenditures, contributed $1.67 billion to the state’s GDP, and created over 12,000 jobs. In the U.S. at large, it estimates bitcoin mining has contributed $10.56 billion in total expenditures, $4.14 billion to GDP, and more than 31,000 jobs.

Market Overview

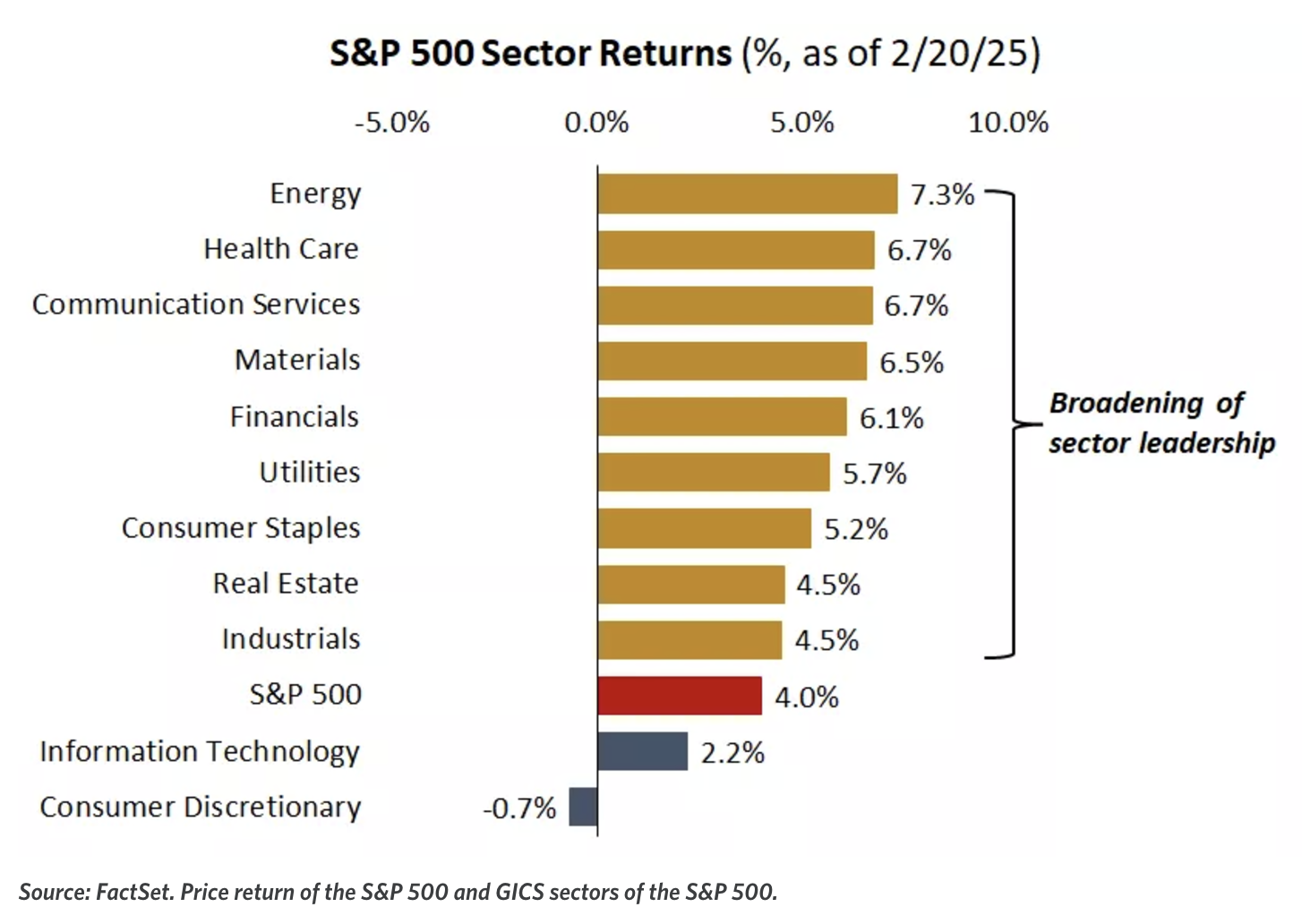

- S&P 500 hits all-time high, while peers come close but end week in the red: Equities rose last week, with the S&P 500 rallying to an all-time high mid-week. The Nasdaq and Dow rose close to their own record highs in the middle of the week, but each index sold off on Friday and closed in the negative.

- S&P 500: 6,013.13 (-1.67%)

- Dow: 43,428.02 (-2.5%)

- Nasdaq: 19,524.01 (-2.5%)

- Russell 2000: 2,195.35 (-3.7%)

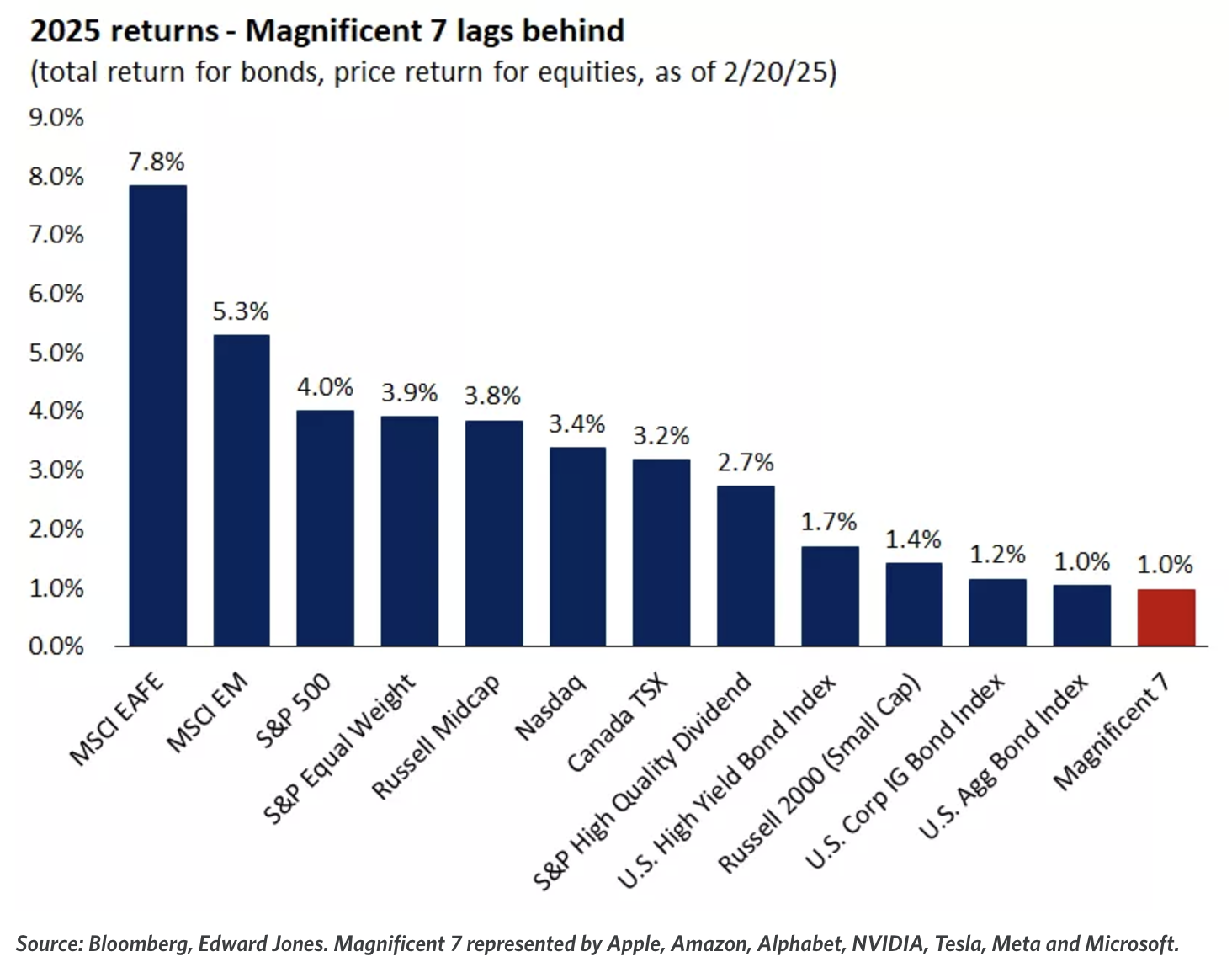

- Magnificent 7 continues to bring up the rear: The Magnificent 7 tech stocks continue to fall behind the broader market, a complete flip of 2024's script. Per analysis from Edward Jones, the Magnificent 7 was responsible for half of S&P 500 returns last year, but total returns for Magnificent 7 bonds and equities year-to-date is only 1%. To explain the lackluster returns, Edward Jones cites tariff vulnerabilities for these global companies, not to mention that they are due for a breather after collectively appreciating some 150% since the outset of 2023.

- Oil slumps while natural gas leaps:

- U.S. oil prices fell for the fifth week in a row last week. WTI Crude closed at $70.17/barrel, a 0.7% decline.

- As of the EIA’s Wednesday update, the March 2025 NYMEX contract for the Henry Hub rose $0.72 from $3.56/MMBtu to $4.28/MMBtu. The rise is largely attributed to a polar vortex that blanketed 35 states with subzero or near-freezing temperatures last week.

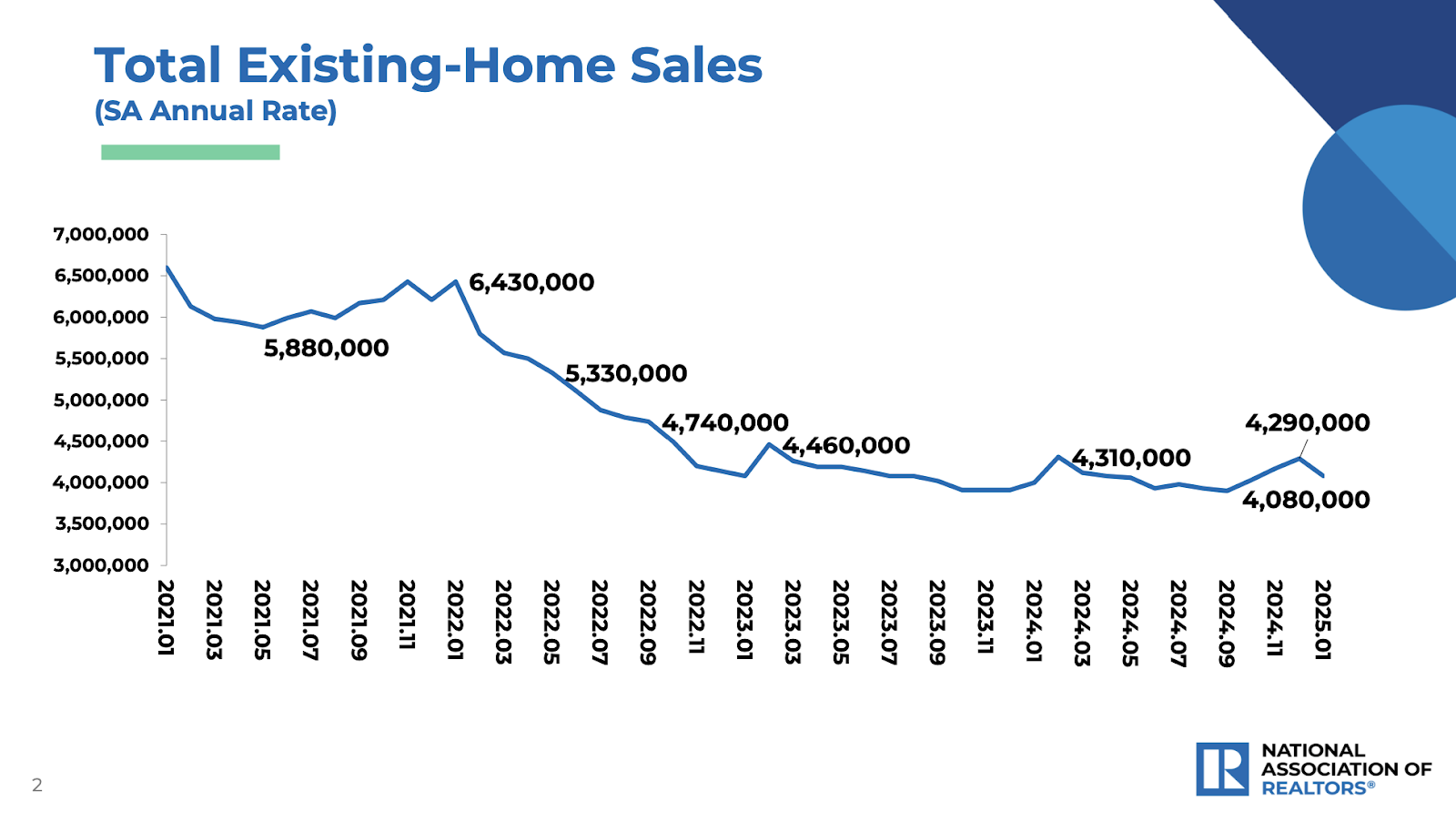

- Home sales fall as home builder confidence, new starts plummet: Existing-home sales dropped 4.9% in January month-over-month, according to the National Association of Realtors, but sales were still up 2% year-over-year. January’s median existing-home sales price rose to $396,900, a 4.8% increase year-over-year.

- Meanwhile, the National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index has fallen to 42 in February, a five point decrease from January and the lowest level since September 2024. Builders cited tariffs, elevated mortgage rates, and cost of labor and materials as the primary factors for declining sentiment. The U.S. Census Bureau reported that new home starts fell 9.8% in January 2025.

- Walmart beats earnings but downscales forward sales guidance: Walmart’s 2024 earnings could be a canary in the coal mine for consumer sentiment. The superstore beat 2024 expectations with $180.6 billion in sales last year, a 5.2% increase. But it also revised down its forward guidance for future net sales increases from 4% to 3-4%. Walmart’s CFO cited uncertainty with tariffs and macroeconomic factors as part of the reason for the revision.

- Walmart’s change in forward guidance reflects drooping consumer sentiment as recorded in the University of Michigan’s latest Index of Consumer Sentiment. The index dropped from 71.1 to 64.7 in January, a 10% drop to the lowest level since July 2024. Fears of tariff-driven price increases and general inflation worries were the primary drivers of the decline in sentiment.

The week ahead in data:

- Chicago Fed National Activity Index (Monday)

- Dallas Fed Manufacturing survey (Monday)

- Case-Shiller Home Price Index (Tuesday)

- Conference Board’s Consumer Confidence Index for February (Tuesday)

- U.S. Census Bureau housing starts report (Wednesday)

- EIA petroleum report (Wednesday)

- Bureau of Economic Analysis U.S. 2024 GDP (Thursday)

- Durable Goods Orders (Thursday)

- Pending Homes Sales Index (Thursday)

- U.S. Department of Labor weekly unemployment claims (Thursday)

- International Trade in Goods, advanced report (Friday)

- U.S. Bureau of Economic Analysis Personal Income and Outlays (Friday)

- Institute for Supply Management PMI (Friday)

Notable corporate earnings this week:

- ONEOK (Monday)

- Realty Income Corporation (Monday)

- Diamondback Energy (Monday)

- Zoom (Monday)

- Home Depot (Tuesday)

- Intuit (Tuesday)

- Nvidia (Wednesday)

- Salesforce (Wednesday)

- Dell (Thursday)

Thank you for reading, and please feel free to reach out with any questions.

Christian Lopez