CCM Blockchain Newsletter (July 7, 2025)

The S&P 500 and Nasdaq reached new highs while bitcoin continued to trade rangebound.

Happy Monday everyone, and welcome back to this week’s market newsletter. Hope that all of our American readers had a relaxing Fourth of July weekend! Please see below this week’s market data.

Bitcoin Market Update and News

- Bitcoin hits $110,000 but ends week mostly flat: Bitcoin rallied to $110,000 on Thursday, only to fall and end the week where it started in the $108,000 range. At the time of publication, Bitcoin is up 0.7% week-over-week to $108,100.

- Senator Lummis introduces bill to exempt de minimis crypto payments from taxes: Sen. Cynthia Lummis (R-WY) has introduced standalone tax legislation that failed to make it into the Big Beautiful Bill that would overhaul Bitcoin/crypto taxation. The bill proposes a de minimis exemption for crypto payments under $300, and it would also allow miners and stakers to only pay taxes once they sell their mining/staking rewards.

- Cango, IREN hit 50 EH/s, join MARA and Cleanspark as first public miners to hit milestone: Newcomer public mining firm, Cango, completed an all-stock transaction at the end of June to add 18 EH/s of turnkey ASIC miners to its fleet, bumping its total active hashrate to 50 EH/s. IREN also reported that it recently passed the 50 EH/s mile marker. MARA and Cleanspark both achieved 50 EH/s respectively in April and June. These four bitcoin miners collectively operate roughly 20-25% of Bitcoin’s total network hashrate.

Interesting Reads and Videos

- Strategy’s Trillion Dollar Bitcoin Bet

- The Nakamoto Strategy: Seeding Bitcoin Treasury Companies in Every Capital

- Summer Curtailments Slash Bitcoin Production for US Miners Amid Grid Pressures

Bitcoin Treasury Updates

- Figma IPO prospectus reveals it owns $70 million in bitcoin ETFs: Designing software mainstay Figma filed for an IPO on the NYSE, and its prospectus reveals that the company owns roughly $70 million in bitcoin ETFs, which makes up 4.5% of its cash and securities holdings. The company’s board approved of the original investment of $55 million in March 2024.

- Strategy buys 4,980 BTC: Strategy has purchased 4,980 BTC for $531.9 million, increasing its overall holdings to 597,325 (worth $65 billion at the time of writing). Strategy raised the cash for the buy by issuing a mixture of common MSTR stock and preferred STRK and STRF stock.

- The Smarter Web company purchases 230 BTC: The UK-based Smarter Web Company has acquired 230.05 BTC for $24.6 million, increasing its total treasury to 773.58 BTC (worth $84.5 million at the time of writing).

Market Overview

- Stocks continue to climb: Equities added to their gains last week, with the S&P 500 and Nasdaq rising above the record highs they set the week before. The Dow is still roughly half a percentage point from the high it set last December.

- S&P 500: $6,279.35 (+2.1%)

- Dow: $44,828.53 (+3%)

- Nasdaq: $20,601.10 (+1.9%)

- Russell 2000: $2,249.04 (+3.3%)

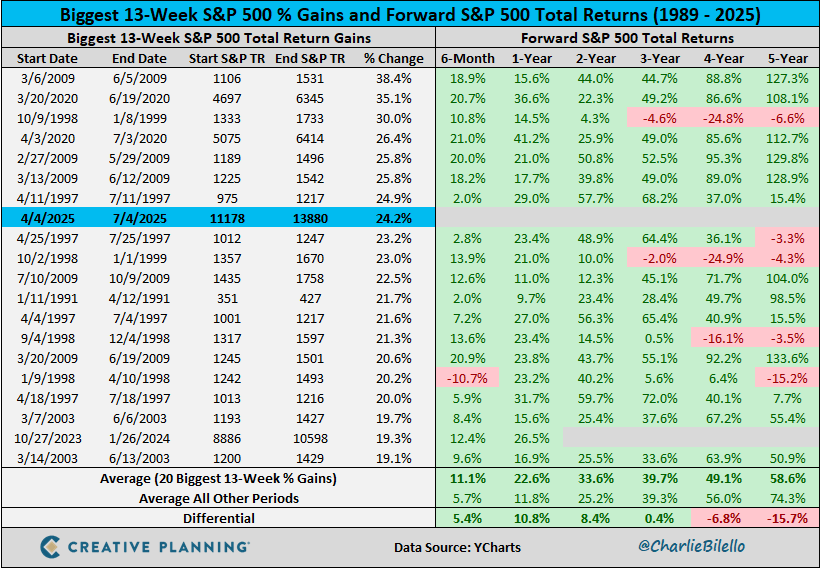

- Stocks shore up April losses to end Q2 on a high note: U.S. equities ended Q2 on a high note despite April’s bloodbath. The S&P 500 ended the quarter up 10.6%, the Nasdaq up 17.8%, and the Dow up 5%. The major indices sold off roughly 14% in April but rebounded impressively in May and June amid AI-driven market momentum and trade negotiations. The S&P 500’s gain over Q2 and into the first week of Q3 is one of the best short term runs in the index’s history.

- Big Beautiful Bill passes House and Senate: The so-called Big Beautiful Bill passed narrowly in the Senate on June 30, with Vice President JD Vance dishing out a tie breaking vote after the bill landed an even 50-50 split. President Trump signed the bill into law on July 4. The sweeping legislation extends 2017’s tax cuts, exempts up to $25,000 in tips from taxes and up to $12,500 in overtime from taxes, and adds $4.5+ trillion in tax provisions. The Congressional Budget Office estimates that the bill could add $2.4-2.8 trillion to U.S. government debt over the next decade.

- June jobs report beats expectations: Nonfarm payroll increased by 147,000 in June, just above the 146,000 12-month average and exceeding expectations of 110,000-120,000. Private sector growth, however, was sluggish, expanding by 74,000 for the lowest growth since October 2024, versus 73,000 for government jobs (of which, 63,000 came from state and local education). The unemployment rate fell to 4.1% from 4.2% in May, partly due to 130,000 people exiting the labor force, while labor force participation stayed at 62.3%. Long-term unemployment (over 27 weeks) rose by 190,000 to 1.6 million, which is 23% of all those unemployed. Average hourly earnings rose 0.2% month-over-month and 3.7% year-over-year.

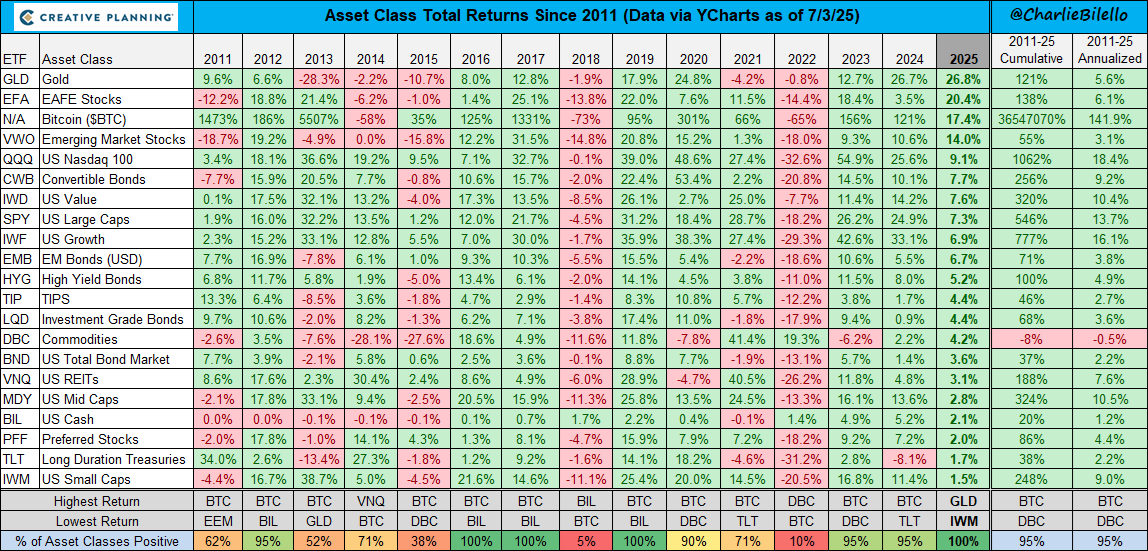

- Every major asset class is positive YTD in 2025: As of market close on July 3, every asset class is now in positive return territory. Gold is leading the charge up 26.8%, followed by EAFE stocks at 20.4% and bitcoin at 17.4%. Preferred stocks (2%), long duration treasuries (1.7%), and U.S. small caps (1.5%) are bringing up the rear.

- Dollar continued to slip in Q2: The DXY got a price pop at the end of last week, but that might be cold comfort when we look at its Q2 and YTD performance. The DXY declined 5.9% in Q2 and it’s down 10.7% in the first half of 2025, the worst H1 decline since the 1970s.

- Bond prices continue to whipsaw: U.S. Treasury Bonds fell last week, driving up yields in both long term and short term bonds and retracing some of the ground bonds made in the opposite direction the week prior. Week-over-week change:

- 2-year: 3.87% (+0.12%)

- 5-year: 3.94% (+0.11%)

- 10-year: 4.35% (+0.06%)

- 30-year: 4.86% (+0.01%)

- Trade deficit widened in May: The U.S. goods and services trade deficit expanded to $71.5 billion in May, up from $60.3 billion in April and a $11.3 billion year-over-year increase (+18.7%). On a goods-only basis, the deficit widened to $96.6 billion, rising 11.1% month-over-month primarily due to falling exports. The deficit widened mainly from a 4% drop in exports, approximately $11.6 billion across goods and services, while import levels remained essentially unchanged.

The week ahead in data:

- Federal Reserve Consumer credit report (Tuesday)

- National Federation of Independent Business Small Business Optimism Index (Tuesday)

- Fed June 17-18 meeting minutes released (Wednesday)

- U.S. Census Bureau wholesale inventories report (Thursday)

- U.S. Department of Labor Statistics jobs and unemployment report (Thursday)

- U.S. Department of Labor Statistics Jobless Claims (Thursday)

- U.S. Treasury federal budget report (Friday)

Notable corporate earnings this week:

- Penguin Solutions (Tuesday)

- AZZ (Wednesday)

- Delta Air Lines (Thursday)

- Conagra Brands (Thursday)

- Levi Strauss & Co (Thursday)

Thank you for reading, and please feel free to reach out with any questions.

Christian Lopez