CCM Blockchain Newsletter (June 10, 2025)

Bitcoin is closing in on $110,000, and equities ended in the green last week for the second week in a row.

Happy Tuesday everyone, and welcome back to this week’s market newsletter. Please see below this week’s market data.

Bitcoin Market Update and News

- Bitcoin flat on the week: Bitcoin essentially traded sidewise last week, dropping to $100,000 before rising to $105,000 to close the week. At the time of publication, Bitcoin is up 2.5% week-over-week to $109,000.

- Circle IPO blows away expectations: Stablecoin and crypto financial services company Circle (CRCL) went public last Thursday, and the market debut shattered expectations. Circle raised just over $1 billion with the IPO at an offer price of $31 per share. Circle surged to over $120 in the day after its IPO, and it closed the week at $107.70, up 247% from its offer price.

- Russia’s largest bank launches Bitcoin-linked bonds: Sberbank, the largest bank in Russia which is also state-owned, has rolled out a bond tied to Bitcoin’s price. The bond tracks Bitcoin’s price in USD and the dollar-ruble exchange rate, so it allows holders to earn yield based on the performance of Bitcoin and the dollar’s performance against the ruble. The bond pays out in rubles and is currently only available to qualified investors over-the-counter. Sberbank’s Bitcoin bond is the first ever Bitcoin-linked structured bond to surface from a major bank.

Interesting Reads and Videos

- THIS TIME IS DIFFERENT: Bitcoin, WALL STREET & ENERGY w/ Harry Sudock

- Trump social-media company seeks Bitcoin ETF

- What you missed at Bitcoin 2025

Bitcoin Treasury Updates

- Blockchain Group buys $69 million in BTC for treasury: The self-proclaimed first Bitcoin treasury company for Europe, Blockchain Group, has purchased 624 BTC for $68.7 million. The company now holds 1,471 BTC worth over $150 million.

- Korean media company K Wave to raise $500 million for Bitcoin treasury: K Wave Media, a Korean media firm that trades on the Nasdaq, has inked a securities purchase agreement with Bitcoin Strategic Reserve KWM LLC to sell up to $500 million in equity. The company plans to use a portion of the proceeds to establish a Bitcoin treasury.

Market Overview

- Stocks rise for the second week in a row: Stocks gained again last week on strong employment numbers for May. Small caps led the rise, and the S&P 500 and Nasdaq are just a few percentage points shy from their record highs.

- S&P 500: $6,000.36 (+1.5%)

- Dow: $42,762.87 (+1.2%)

- Nasdaq: $19,529.95 (+2%)

- Russell 2000: 2,132.25 (+3.2%)

- Job market just beats expectations in May: The U.S. Bureau of Labor Statistics released May’s jobs and unemployment report on Friday, and the results just barely beat expectations. The U.S. added 139,000 jobs in May, while unemployment held at 4.2%. The bureau revised down March and April’s numbers, however, cumulatively reducing 95,000 jobs from the originally reported combined figures for both months. The year-to-date average monthly job gain was 124,000, down from 168,000 in 2024, and the labor force participation rate drooped to 62.4%, a three-month low.

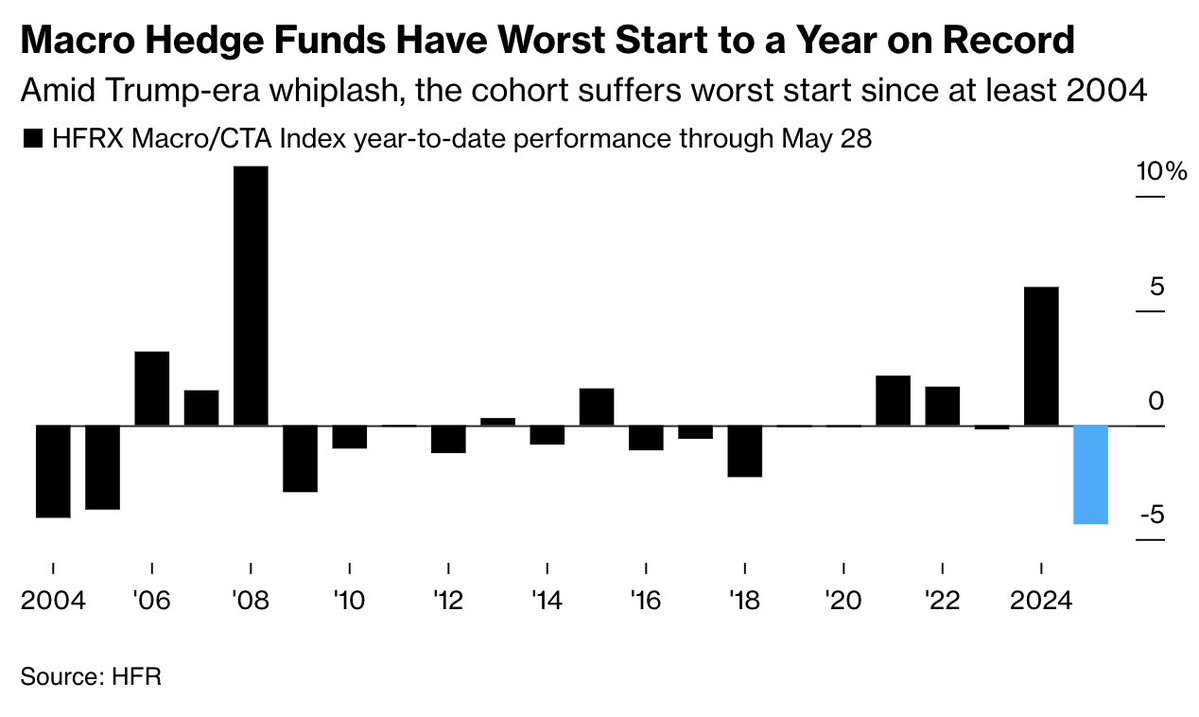

- 2025 is the worst start for macro hedge funds in at least 20 years: As reported by Bloomberg, macro hedge funds are off to a rocky start in 2025 – the worst in over two decades. As of May 28, these hedge funds were down nearly 5%, according to data from Hedge Fund Research, and they lost 2.7% in April. Hedge funds are reportedly having trouble reacting to price dislocation across asset classes and 2025’s whipsaw reversals in market conditions.

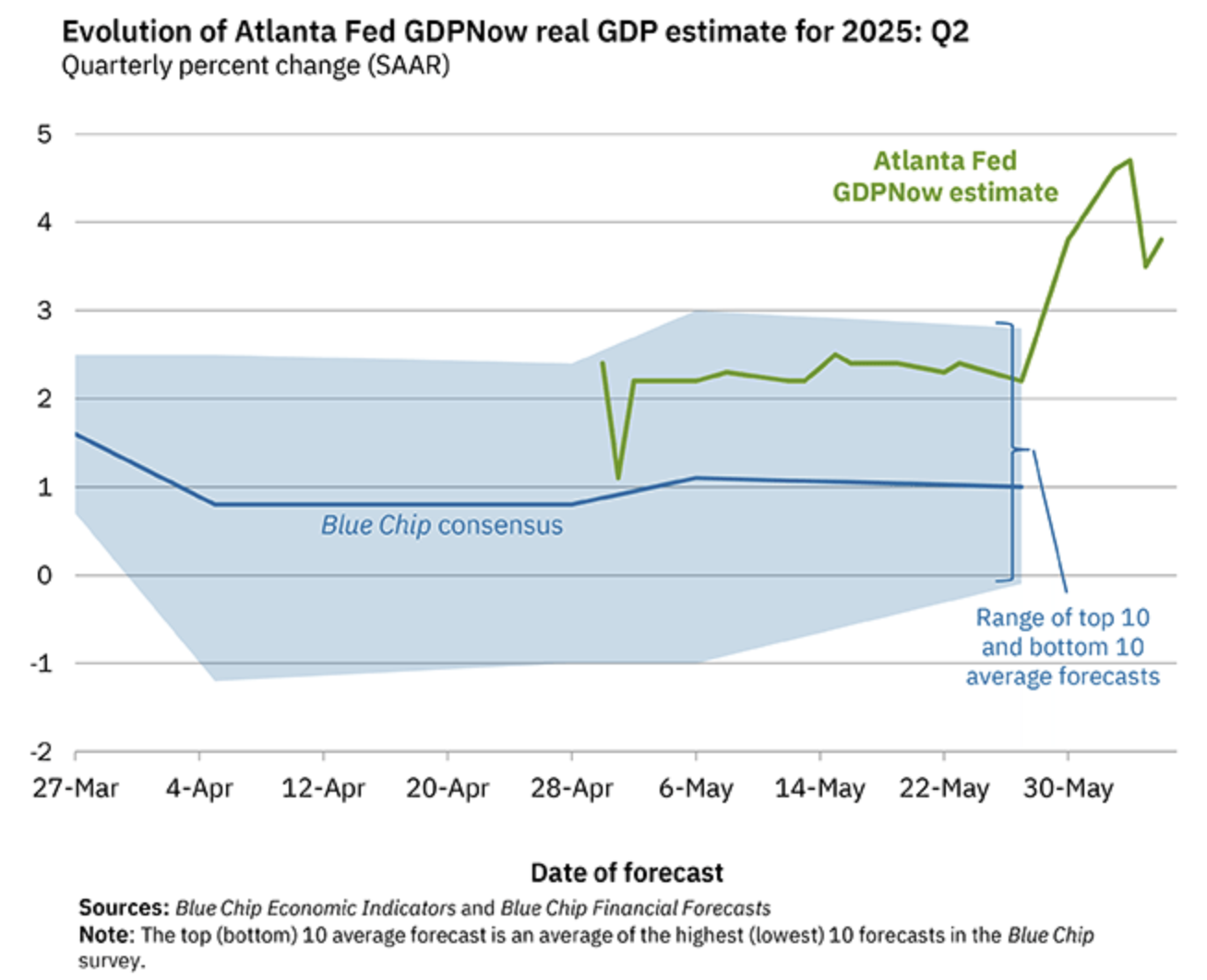

- Atlanta Fed GDPNow forecast now 3.8% for Q2: The Atalanta Federal Reserve's GDPNow forecast for Q2’s annualized GDP now reads 3.8% after peaking at 4.6% on June 2. The Atlanta Fed projects a 4% consumption growth and 0.5% growth in gross domestic private investment. The revision was driven by May’s strong ISM Manufacturing Index report, which pointed to expanding factory activity; strong construction spending in April, both in residential and nonresidential sectors; growth in personal consumption in April; and an increase in exports compared to imports so far in Q2, versus a steep export deficit in Q1.

- Oil surges: Oil prices rose last week for the first time in three weeks as negotiations improved the outlook for U.S.-China trade relations. WTI Crude rose 4% to $63.17/barrel and Brent Crude increased 2.1% to $65.15/barrel.

- Market no longer pricing in rate cut for June or July: A few months ago, markets were fully pricing in a rate cut at the Fed’s June 18 meeting, but now those odds have completely evaporated. Markets are also betting that the Fed will keep rates steady on the July 30 meeting, but they are pricing in a rate cut in September at just over 50%.

The week ahead in data:

- U.S. Census Bureau wholesale inventories index (Monday)

- National Federation of Independent Businesses Small Business Optimism Index (Tuesday)

- U.S. Bureau of Labor Statistics CPI (Wednesday)

- U.S. Department of the Treasury Federal Budget (Wednesday)

- Institute of Supply Management nonmanufacturing index (Wednesday)

- U.S. Department of Labor weekly unemployment report (Thursday)

- U.S. Bureau of Labor Statistics Producer Price Index (Thursday)

- University of Michigan Index of Consumer Sentiment (Friday)

Notable corporate earnings this week:

- VinFast Auto Ltd (Monday)

- Calavo Growers (Monday)

- Casey’s General Stores (Monday)

- GameStop (Tuesday)

- Academy Sports & Outdoors (Tuesday)

- Core & Main (Tuesday)

- J.M. Smucker (Tuesday)

- United Natural Foods (Tuesday)

- GitLab (Tuesday)

- Oracle (Wednesday)

- Chewy (Wednesday)

- SailPoint (Wednesday)

- Cognyte Software (Wednesday)

- Adobe (Thursday)

- Restoration Hardware (RH) (Thursday)

Thank you for reading, and please feel free to reach out with any questions.

Christian Lopez