CCM Blockchain Newsletter (June 17, 2025)

Markets were rocked last week by direct military action between Israel and Iran.

Happy Tuesday everyone, and welcome back to this week’s market newsletter. Please see below this week’s market data.

Bitcoin Market Update and News

- Bitcoin flat (again) on the week: Bitcoin remained essentially flat last week, despite a rally in the early part of the week to nearly $110,000 that was cut short by military tensions in the Middle East. At the time of writing, bitcoin is down 4.8% week-over-week to $104,700.

- GENIUS Act is one step closer to reality: A senate bill that has sweeping ramifications for stablecoins has cleared another congressional hurdle. Last week, the U.S. Senate voted 68–30 to invoke cloture on the GENIUS Act, successfully overcoming the possibility of a filibuster and clearing the way for a final vote in the Senate. Among other things, the bill mandates that stablecoin issuers hold reserves in Treasuries, money market funds, and other perceived safe assets and provides state and federal regulatory clarity.

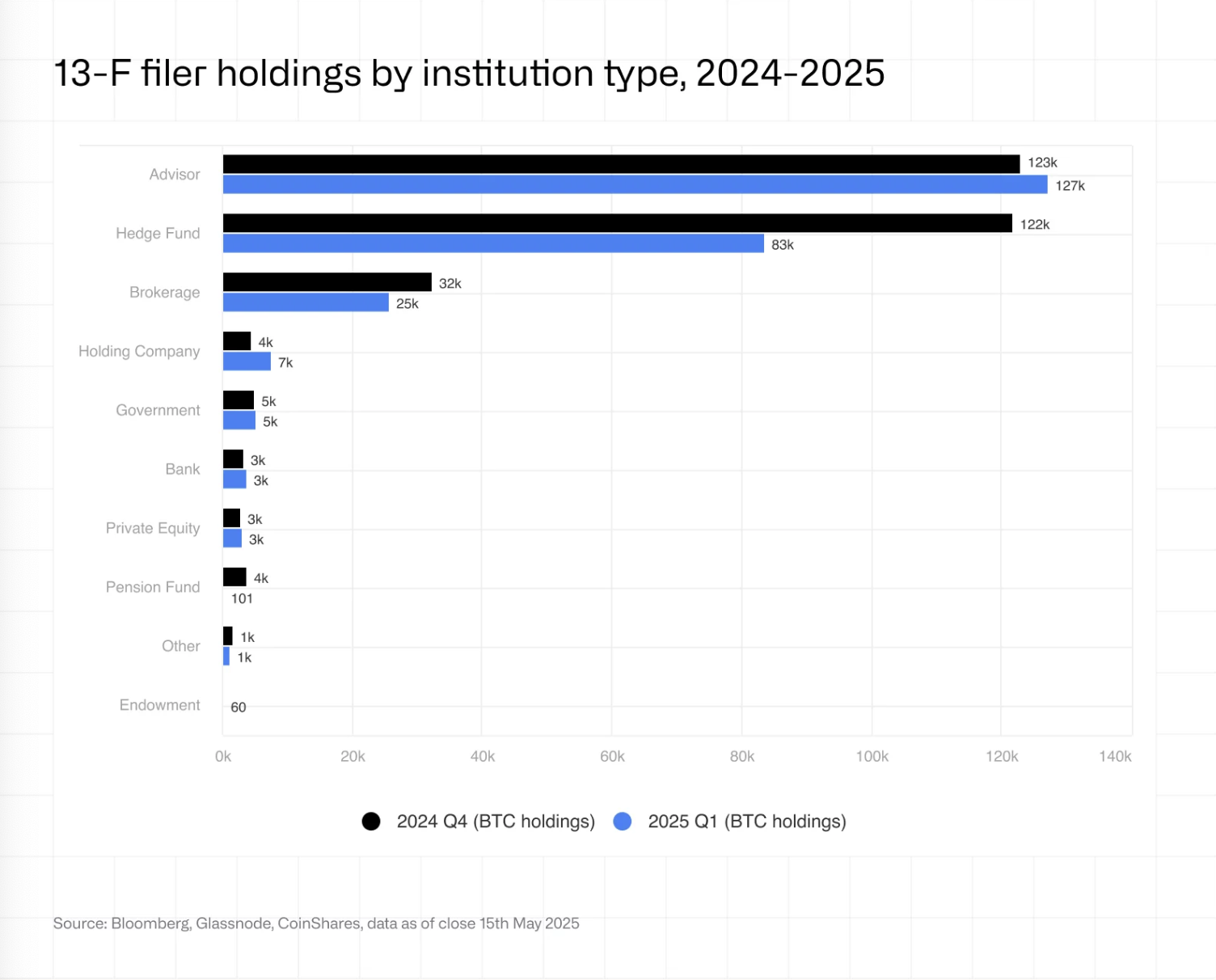

- Institutional bitcoin ETF holdings fell last quarter as hedge funds cycle trades: Institutional holdings of bitcoin ETFs declined by 23% last quarter on a dollar-denominated basis. Of course, bitcoin’s 11% decline over the quarter partly explains the drop, but hedge funds are another culprit in the decline. The collective BTC-denominated holdings of SEC-reporting hedge funds fell from 122,000 to 83,000 over Q1 as the bitcoin basis trade unwound and hedge funds cycled out of bitcoin. Meanwhile, shares of holdings from financial advisors rose from 123,000 to 127,000 BTC.

Interesting Reads and Videos

- THIS TIME IS DIFFERENT: Bitcoin, WALL STREET & ENERGY w/ Harry Sudock

- Trump social-media company seeks Bitcoin ETF

- What you missed at Bitcoin 2025

Bitcoin Treasury Updates

- SEC approves Trump Media’s $2.3 billion capital raise: The SEC green lit Trump Media’s (DJT) $2.3 billion fundraising push via equity and convertible debt offerings. President Trump’s media company plans to use part of the proceeds to purchase bitcoin. The company also has $759 million in cash and short term investments it could use toward building its bitcoin treasury.

- Gamestop announces additional $2.25 billion convertible note issuance: GameStop is looking for more fuel for its bitcoin treasury. The company filed for a $1.75 billion convertible note offering last Wednesday, later upsizing this to $2.25 billion on Thursday with an additional $450 million in potential issuance. The company purchased 4,710 BTC between May 3 and June 10, and investors have speculated that it will use the convertible note issuance to purchase more. “GameStop intends to use the net proceeds from the offering for general corporate purposes, including making investments in a manner consistent with GameStop’s Investment Policy and potential acquisitions,” the press release said.

Market Overview

- Stocks slip to end the week: Equities ended last week marginally in the red, putting an end to the previous two week streak of gains. Stocks sold off sharply on Friday as news of Israel’s military strikes in Iran roiled markets.

- S&P 500: $5,976.97 (-0.4%)

- Dow: $42,197.79 (-1.3%)

- Nasdaq: $19,406.83 (-0.6%)

- Russell 2000: 2,1000.51 (-1.5%)

- Investors flock to safe haven assets amid Israel-Iran conflict: Israel’s strikes on Iran’s nuclear facility and key personnel – and Iran’s subsequent retaliation with missile strikes on Tel Aviv – spooked investors last week. As two of the Middle East’s principal players careen toward outright war, U.S. and international stocks sold off last week, with travel and airline stocks taking particularly large hits. Meanwhile, defense and military stocks surged, gold hit an all-time high of ~$3,470/oz, oil jumped 13%, and the U.S. dollar and Treasuries both rallied as investors flocked to safety.

- WTI crude closed at $72.98/barrel, up 13% week-over-week, while Brent crude closed up 12.5% to $74.23/barrel.

- The DXY rose on Friday following the news after setting its lowest level since 2022 on Thursday. Even with the rally, the dollar was still down 1% last week.

- U.S. and China inch closer to trade deal: American and Chinese officials met in London last week to continue work on brokering a trade deal. Officials agreed on a handshake deal that would place U.S. tariffs on Chinese goods at 55% and Chinese tariffs on U.S. goods at 10%. The deal also includes a six month provision for China to continue to provide rare earth minerals and magnets.

- U.S. house listings hit $698 billion: According to Redfin, there are $698 billion worth of homes for sale in the U.S., the largest figure since Redfin started tracking the data in 2012. This figure represents a 20.3% increase from a year earlier as active listings have grown 16.7% year-over-year. Per Redfin’s report, toughly 44% of homes have remained on the market for over 60 days, resulting in $331 billion of stale inventory.

- May CPI more-or-less unchanged in May: May’s CPI print showed inflation moderating somewhat, although it was still above the Fed’s 2% target. Core inflation came in at 0.1% month-over-month and 2.8% annually, while headline inflation came in at 0.1% and 2.4%. Shelter and rent and food were up 0.3% in May from April, while energy was down 1% and used and new cars both fell 0.5%. Major appliances saw one of the largest monthly increases at 4.3%. Markets expect the Fed to keep rates unchanged in June.

- Consumer sentiment perks up in May: The University of Michigan’s Index of Consumer Sentiment rose to 60.5 in June, up from 52.2 in May. The 16% month-over-month increase is the index’s first gain in six months. Even so, sentiment is still 20% below its December 2024 level.

- Services PMI contracts in May: The Institute of Supply Management’s composite Non-Manufacturing PMI fell to 49.9 in May from 51.6 in April, a drop below the 50 threshold that typically indicates economic contraction. The business activity index hovered at 50, the new orders index declined below 50 for the first time in roughly a year, and the price index hit its highest level since November 2022. The employment index, however, expanded marginally, indicating modest strength in hiring.

The week ahead in data:

- U.S. Census Bureau retail sales report (Tuesday)

- U.S. Federal Reserve industrial production and capacity report (Tuesday)

- U.S. Census Bureau business inventories report (Tuesday)

- National Association of Home Builders Housing Market Index (Tuesday)

- Fed press conference (Wednesday)

- U.S. Census Bureau housing starts (Wednesday)

- U.S. Department of Labor weekly unemployment claims (Wednesday)

- The Conference Board Leading Economic Index (Friday)

- Federal Reserve balance sheet report (Friday)

Notable corporate earnings this week:

- Lennar Corporation (Monday)

- Digital Turbine (Monday)

- Jabil (Tuesday)

- Progressive (Wednesday)

- Smith & Wesson Brands (Wednesday)

- Kroger (Friday)

- Accenture (Friday)

- Darden Restaurants (Friday)

- CarMax (Friday)

Thank you for reading, and please feel free to reach out with any questions.

Christian Lopez