CCM Blockchain Newsletter (June 23, 2025)

Last week, equities had mixed returns and bonds rallied as tensions flared in the Middle East.

Happy Monday everyone, and welcome back to this week’s market newsletter. Please see below this week’s market data.

Bitcoin Market Update and News

- Bitcoin ends choppy week with retreat to $100,000: Bitcoin rallied to $100,800 on Monday, only to stair step its way down to $100,000 by the weekend. At the time of writing, Bitcoin is down 1.2% on the week to $105,500.

- GENIUS Act passes in the Senate: The U.S. Senate passed the GENIUS Act with bipartisan support last week in a 68-30 vote, and the bill is now on its way to the House. The sweeping bill would institute seminal guardrails and regulations for stablecoins, including requiring a 1-to-1 backing with dollars and/or short-term Treasuries, assigning oversight to banking regulators, and mandating security and anti-money laundering requirements.

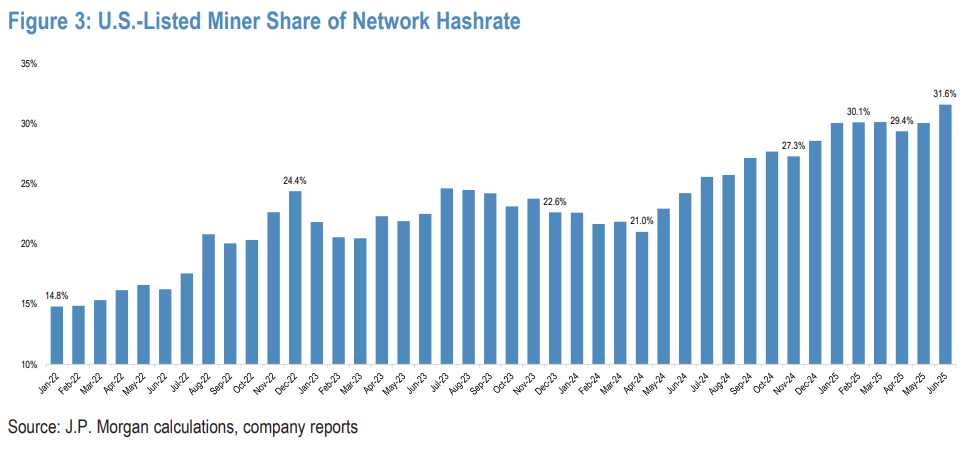

- U.S.-listed Bitcoin miner hashrate share hits record 31.6%: U.S.-listed public Bitcoin miners now control more hashrate than ever before. According to a report from JPMorgan, the 13 largest public miners now command 31.6% of Bitcoin’s total network hashrate, up from 14.8% in January 2022 when JPMorgan’s dataset begins.

Interesting Reads and Videos

- Is Bitcoin Failing? | Alex Gladstein vs. Paul Sztorc

- What Happens to Bitcoin When Quantum Computers Arrive?

- Bitcoin ATM: The best BTC business you’ve never heard of

Bitcoin Treasury Updates

- Anthony Pompliano Strikes $1 Billion Merger to Create ProCap Financial: ProCap BTC, a bitcoin-native financial services firm, has entered into a definitive agreement for a business combination with Columbus Circle Capital Corp. I (NASDAQ: CCCM). At the closing of the proposed business combination, the combined company will have up to $1 billion in bitcoin on its balance sheet.

- Nakamoto Holdings raises additional $51.5 million: Nakamoto Holdings has followed up its historic $710 million raise with a $51.5 million private placement. The company has now raised over $760 million for its Bitcoin treasury strategy as it awaits the completion of its merger with KindlyMD.

- Smarter Web Company adds 104 BTC to balance sheet: The U.K. listed Smarter Web Company has purchased 104.28 BTC for $10.89 million, upping its Bitcoin treasury to 346.63 BTC.

- Strategy buys $1.05 billion in Bitcoin: Strategy reported last week that it purchased 10,100 BTC between June 9 and 15 for $1.05 billion. The company now holds 592,345 BTC – 2.9% of Bitcoin’s circulating supply.

Market Overview

- Stocks end week with mixed returns: Equities provided mixed returns last week, with the S&P 500 declining for the third week in a row while other major indices saw minimal gains.

- S&P 500: $5,967.84 (-0.2%)

- Dow: $42,206.82 (+0.1%)

- Nasdaq: $19,447.41 (+0.2%)

- Russell 2000: $2,123.40 (+1.1%)

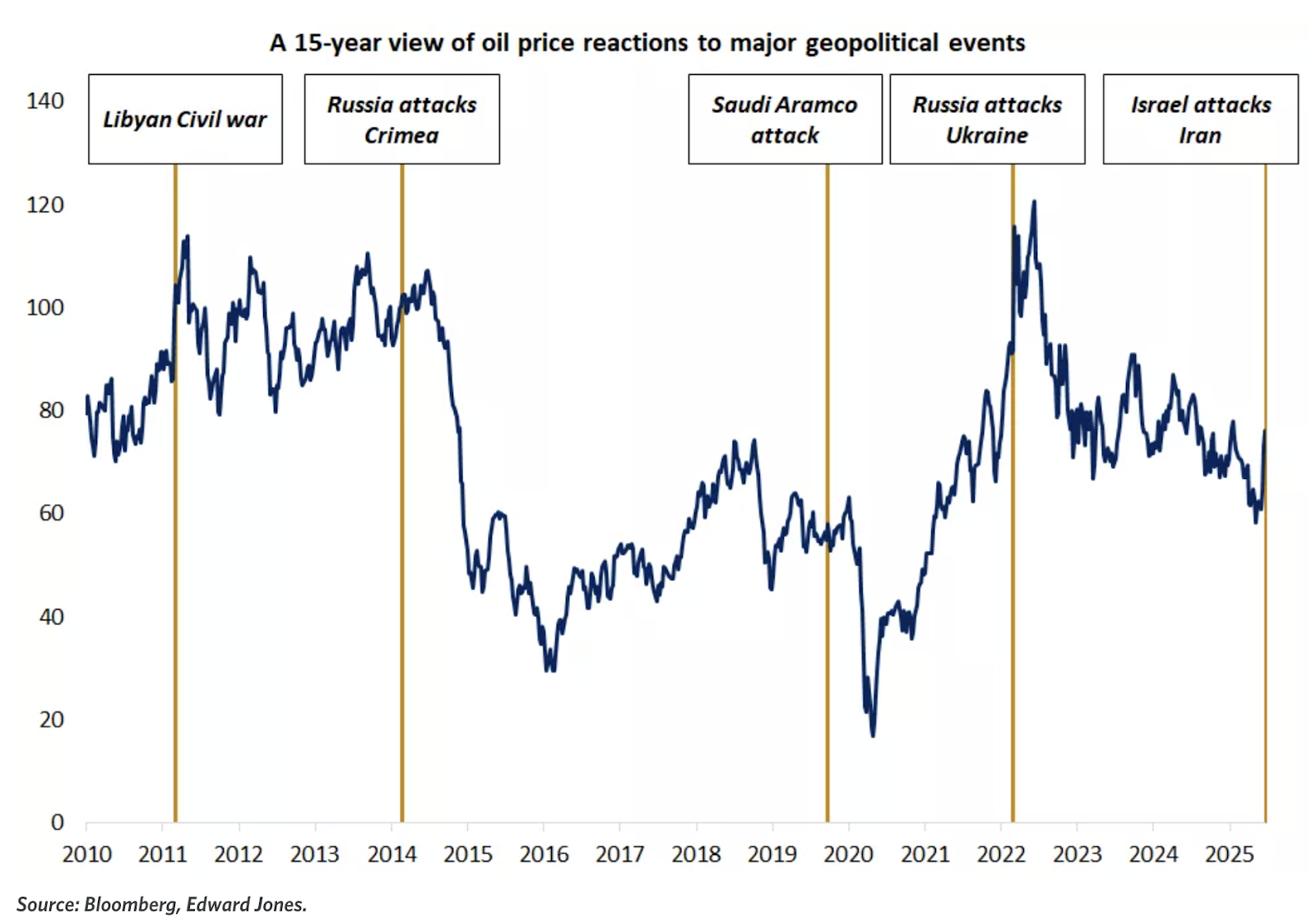

- Oil continues to climb: Oil prices ticked further up last week, adding to the prior week’s surge as markets reacted to the Israel-Iran war. WTI Crude closed up 3.8% at $74.04/barrel and Brent Crude closed up 3.1% at $72.40/barrel. Oil prices rose in after hour trading over the weekend after the U.S. conducted airstrikes against Iran’s nuclear bases.

- Fed keeps interest rates unchanged: The Federal Open Market Committee agreed during last week’s policy meeting to keep the federal fund rate unchanged. Fed Chair Jerome Powell said the Fed won’t rush to cut rates, noting a strong labor market, stubborn inflation, expectations for the Trump Administration’s tariffs to stoke inflation further, and fears of stagflation. The Federal Reserve now estimates 3.1% headline PCE inflation for 2025, up from 2.7% in March. Markets are now pricing in two rate cuts in 2025, one in September and another in December.

- Bond market rallies modestly on Fed news, tensions in Middle East: U.S. Treasury Bonds rose last week, pushing yields down as investors reacted to the Fed’s decisions to leave rates unchanged and rising tensions in the Middle East.

- 30-year: 4.89% (-0.01%)

- 10-year: 4.38% (-0.03%)

- 5-year: 4.02% (-0.06%)

- 2-year: 3.96 (-0.06%)

- Housing starts drop to lowest level since pandemic: Total housing starts in the U.S. slipped to an annual pace of 1,256,000 in May, a 9.8% monthly decrease and 4.6% annual decrease. Single family home starts increased 0.4%, while multi-family home starts plunged by 30%. The strongest headwinds include high construction costs, tariffs on raw materials, elevated mortgage rates, and rising inventories of unsold homes.

- NAHB Housing Market Index reveals flagging confidence in early June read: The National Association of Home Builders Housing Market Index for June betrays limping expectations from construction firms. The builder confidence index has hit 32 so far in June, down from 34 in May and the lowest since December 2022. The current sales index drooped to 35, the future six-month expectations index fell to 40, and the buyer traffic index hit 21 – the lowest since November 2023. 37% of builders reduced prices in June, with an average cut of 5%, while 62% offered buyer incentives.

- Conference Board warns of recession signals in latest report: The Conference Board’s Leading Economic Index slipped 0.1% in May to 99.0, the sixth consecutive monthly decline. Over the past six months, the LEI has fallen 2.7%, a faster pace than the previous period and enough to trigger the Conference Board’s recession warning signal. While the stock market rebounded in May, the Conference Board cited weak manufacturing orders, consumer pessimism, rising unemployment claims, and housing permit declines as drags on the index.

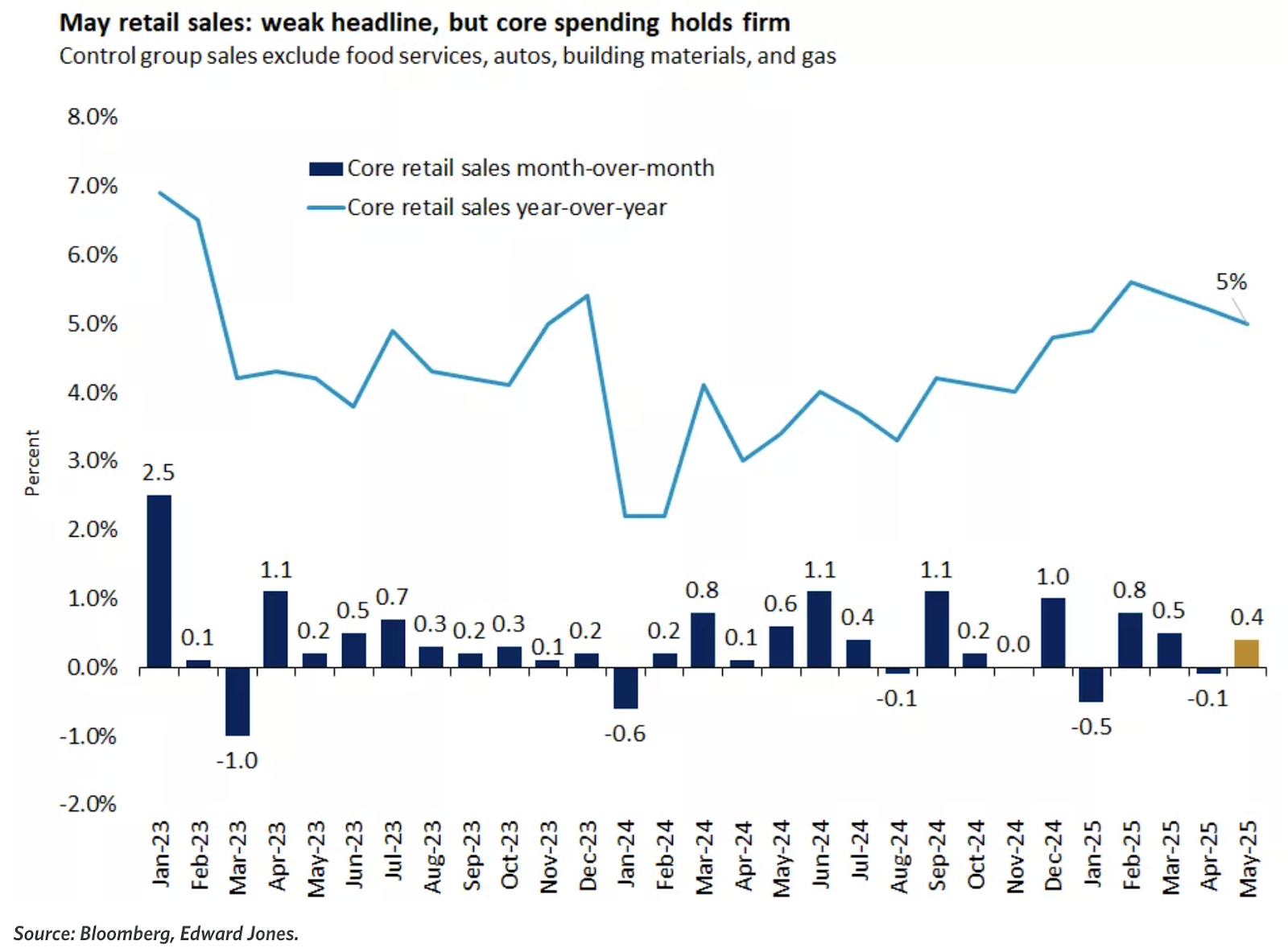

- Retail sales cool in May: The U.S. Census Bureau’s retail sales report for May revealed that Americans are cooling off on tariff-induced panic buying. Total retail and food services sales dropped 0.9%, the steepest decline since January and the second consecutive monthly decline. Still, total retail sales were up 3.3% year-over-year at $715.4 billion. Auto and parts dealers, building materials and garden equipment, and grocery and restaurant sales respectively fell 3.5%, 2.7%, and 0.3%. Core retail sales grew 0.4% month-over-month and ecommerce sales grew 8.3% year-over-year.

The week ahead in data:

- National Association of Realtors Existing Home Sales (Monday)

- Case-Shiller Home Price Index (Tuesday)

- Federal Housing Finance Agency House Price Index (Tuesday)

- Conference Board Consumer Confidence Index (Tuesday)

- Richmond Federal Reserve Manufacturing Index (Tuesday)

- U.S. Census Bureau New Home Sales (Wednesday)

- GDP read (Thursday)

- U.S. Census Bureau Durable Goods Orders (Thursday)

- U.S. Census Bureau International Trade in Goods report (Thursday)

- Kansas City Federal Reserve Manufacturing Index (Thursday)

- National Association of Realtors Pending Home Sales Index (Thursday)

- U.S. Department of Labor Jobless Claims (Thursday)

- U.S. Bureau of Economic Analysis Personal Income and Outlays report (Friday)

- University of Michigan Consumer Sentiment report (Friday)

Notable corporate earnings this week:

- Commercial Metals Company (Monday)

- FactSet Research Systems (Monday)

- FedEx (Tuesday)

- Micron Technology (Wednesday)

- General Mills (Wednesday)

- Nike (Thursday)

- Walgreens (Thursday)

Thank you for reading, and please feel free to reach out with any questions.

Christian Lopez