CCM Blockchain Newsletter (June 30, 2025)

The S&P 500 and Nasdaq hit all-time highs last week while bitcoin eyed $110,000.

Happy Monday everyone, and welcome back to this week’s market newsletter. Please see below this week’s market data.

Bitcoin Market Update and News

- Bitcoin rises, eyes $110,000: Bitcoin rallied to $107,000 by Friday and rose slightly throughout the weekend before retracing at the beginning of this week. At the time of writing, Bitcoin is up 2% week-over-week to $107,200.

- CoreWeave in talks to acquire Core Scientific: As first reported by the Wall Street Journal, cloud computing company CoreWeave (Nasdaq: CRWV) is in advanced talks to buy Core Scientific (Nasdaq: CORZ) , the Bitcoin miner-turned AI infrastructure provider which is currently CoreWeave’s largest infrastructure partner with 590 MW under contract. Sources told WSJ that the deal could close in a matter of weeks. Cantor Fitzgerald estimates that, on the higher end, the acquisition could fetch $30/share ($8.9 billion). Core Scientific shares surged 33% on the news.

- FHFA orders Fannie Mae and Freddie Mac to recognize crypto as a legitimate asset for mortgages: The Federal Housing Finance Agency issued an order this week for Fannie Mae and Freddie Mac to create proposals for considering cryptocurrencies as legitimate assets when assessing the financial health of single-family mortgage borrowers. The order specifically mentions that only cryptocurrencies held on regulated exchanges or custodians should be considered.

Interesting Reads and Videos

- What Antalpha’s loan book can tell us about its relationship with Bitmain

- The Bitcoin Legislative Agenda in the US Senate | 2025 Bitcoin Policy Summit

- Legislative Prospects for the SBR with Whip Emmer & Rep. Begich | 2025 Bitcoin Policy Summit

- Cantor Fitzgerald sees $30/share acquisition price in CoreWeave deal

Bitcoin Treasury Updates

- Metaplanet buys 1,234 BTC, holdings are now 12,345 BTC: Metaplanet (TSE: 3350; OTCMKTS: MTPLF) keeps adding to its Bitcoin stack. Last week, the Japanese MicroStrategy purchased 1,234 BTC for $133 million dollars. The company now holds 12,345 BTC ($1.32 billion), and it says that it is targeting to own 210,000 BTC by the end of 2027.

- Coinbase starts building its Bitcoin treasury: The U.S.’s largest crypto exchange, Coinbase (Nasdaq: COIN), is finally getting into the treasury game. CEO Brian Armstrong revealed this week that the company is buying Bitcoin weekly and currently holds 9,257 BTC ($990 million).

- A host of newcomer Bitcoin treasury companies enter the arena:

- Canada’s first bitcoin treasury company, the aptly named Bitcoin Treasury Corp (TSX-V: BTCT), relisted on the Toronto Stock Exchange, raised $91.16 million, and bought 292.8 BTC ($31.38 million).

- The board of Chinese software and services company Aurora Mobile (Nasdaq: JG) authorized converting up to 20% of the company’s cash into bitcoin.

- U.K. tech firm Vinanz Ltd. (LSE: BTC.L) bought 5.85 ($626.9k) BTC to increase treasury to 65 BTC ($7 million).

Market Overview

- Stocks are back on top: Equities surged last week following positive trade talks and easing military tensions in the Middle East. The S&P 500 and Nasdaq hit record highs, while the Dow is still a few percentage points away from its December all-time high.

- S&P 500: $6,173.07 (+3.4%)

- Dow: $43,819.27 (+3.9%)

- Nasdaq: $20,273.46 (+4.4%)

- Russell 2000: $2,172.53 (+3.2%)

- Trump administration makes headway on trade talks with China ahead of July 9 deadline: As the July 9 deadline for the resumption of Trump’s reciprocal tariff schedule approached, the U.S. has made progress with key trading partners while stalling with others. The U.S. and China have finalized a deal that would involve a 55% tariff on Chinese goods in the U.S. and a 10% tariff on U.S. goods in China, as well as the resumption of Chinese exports of rare earth minerals to the U.S. Meanwhile, talks with Canada have stalled, with President Trump criticizing Canada’s digital service tax as a “blatant attack” on U.S. businesses. Additionally, negotiations with India have stagnated over disagreements regarding auto, steel, and agricultural goods.

- May inflation ticks higher: Last week’s PCE inflation read for May came in above the Fed’s 2% target and expectations. Headline PCE rose 0.1% month-over-month and 2.3% year-over-year, while Core CPE increased 0.2% MoM and 2.7% YoY. Personal income declined 0.4% and disposable personal income fell 0.6%, the first decline since September 2021, and the personal savings rate stood at 4.5% versus 4.9% in April. So far, tariff pressures have only impacted inflation moderately.

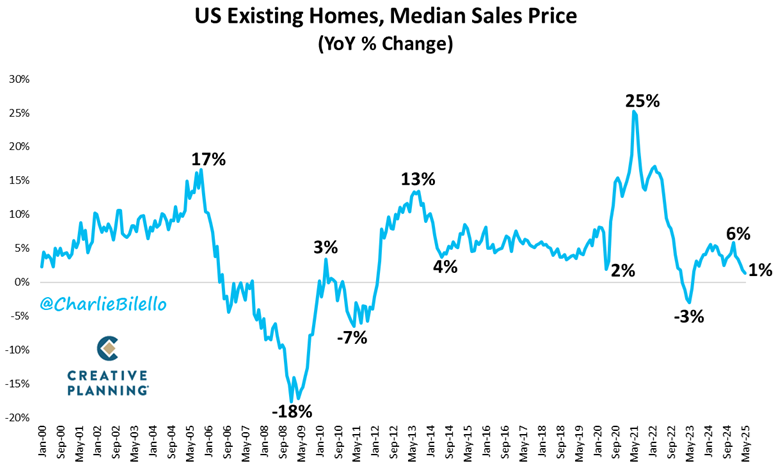

- Series of reports point to cooling demand in housing market while housing prices are at or near all-time highs: Last week, the U.S. Census Bureau, the Federal Housing Finance Agency, and the National Association of Realtors all released indices or reports that reaffirm cooling trends in U.S. realty.

- U.S. Census Bureau New Homes Sales: Seasonally adjusted annual sales dropped 13.7% MoM and 6.3% YoY to 623,000 units. Inventory surged to 507,000 homes or 9.8 months of supply – the highest since late 2007. New home sales in the South fell the most, plunging by 21%. Despite these trends, the median home price rose to $426,000, a 3.7% increase MoM and 3.3% YoY.

- FHFA Housing Price Index for Q1 2025: U.S. single-family home prices were up 0.7% QoQ and 4.0% YoY as of Q1. Every U.S. state experienced annual gains, led by states in the Middle Atlantic.

- National Association of Realtors Home Sales Index for May: Pending home contracts rose 1.8% MoM and 1.1% YoY. All four regions tracked by the association saw month-over-month price increases, while the Northeast and the West experienced annual declines.

- U.S. manufacturing activity still in contraction: The Kansas City and Richmond Feds both released reports on the U.S. manufacturing industry that point to contracting activity, while also including optimistic indicators for future growth. The Kansas City survey’s composite activity of June marked 22 straight months of contraction, although the -2 read was a slight improvement from May’s -3 and April’s -4; meanwhile, the future outlook rebounded to +9 from +5 in May. Richmond’s composite index for June rose from -9 in May to -7. Both surveys cited higher pricing pressures on raw materials and finished goods.

- Final Q1 GDP read shows larger contraction than expected driven by expedited imports: The U.S. Treasury's final Q1 2025 GDP read came in at -0.5%, versus +2.4% in Q4. The contraction is deeper than earlier estimates of -0.2% and it follows a slew of pulled-ahead imports from U.S. firms that tried to outrun the Trump Administration’s tariff regime. That said, private domestic final purchases grew 2.5% as business investment remained resilient. The Atlanta Fed’s GDPNow forecast anticipates a Q2 GDP rebound to 2.9%.

- Bond prices rise as trade negotiations progress, geopolitical tensions cool: U.S. Treasury Bonds increased last week, driving down yields in both longterm and shorterm bonds. An improved geopolitical backdrop – both with U.S. trade deal talks and easing tensions in the Middle Easts – gave bonds a boost, while falling short term yields could also indicate that investors expect the Federal Reserve to cut interest rates sooner then later. Week-over-week changes:

- 2-year: 3.75% (-0.21%)

- 5-year: 3.83% (-0.13%)

- 10-year: 4.29% (-0.09%)

- 30-year: 4.85% (-0.04%)

- Personal income, spending fall in May: The U.S. Bureau of Economic Analysis’ Personal Spending and Outlays report for May indicated a slowdown in both consumer spending and personal income. Personal income decreased by 0.4%, a decline of $109.6 billion driven largely by reduced Social Security benefits and lower farm income, while disposable personal income fell by 0.6%. Nominal personal consumption dropped 0.1%, the second such this year, and real personal consumption fell 0.3%. Wages and salaries increased moderately by 0.4%.

The week ahead in data:

- Chicago Purchasing Managers Index (Monday)

- U.S. Department of Labor Statistics Job Openings and Labor Turnover Survey (Tuesday)

- Institute for Supply Management’s manufacturing index (Tuesday)

- U.S. Census Bureau construction spending (Tuesday)

- ADP National Employment Report (Wednesday)

- U.S. Census Bureau factory orders report (Thursday)

- U.S. Department of Labor Statistics jobs and unemployment report (Thursday)

- Institute for Supply Management nonmanufacturing index (Thursday)

- U.S. Census Bureau trade balance report (Thursday)

- U.S. Department of Labor Statistics Jobless Claims (Thursday)

Notable corporate earnings this week:

- Quantum Corporation (Monday)

- Jeffs’ Brands Ltd (Monday)

- Kaixin Auto Holdings (Monday)

- Rail Vision Ltd (Monday)

- JFB Construction Holdings (Monday)

- Asia Pacific Wire & Cable (Monday)

- Ellomay Capital Ltd (Monday)

- Progress Software (Monday)

- MSC Industrial (Tuesday)

- Constellation Brands (Tuesday)

- Greenbrier (Tuesday)

Thank you for reading, and have a great Fourth of July weekend! Please feel free to reach out with any questions.

Christian Lopez