CCM Blockchain Newsletter (March 3, 2025)

Every corner of the market, from equities to bitcoin, saw red last week.

Happy Monday everyone, and welcome back to this week’s market newsletter. Please see below this week’s market data.

Bitcoin Market Update and News

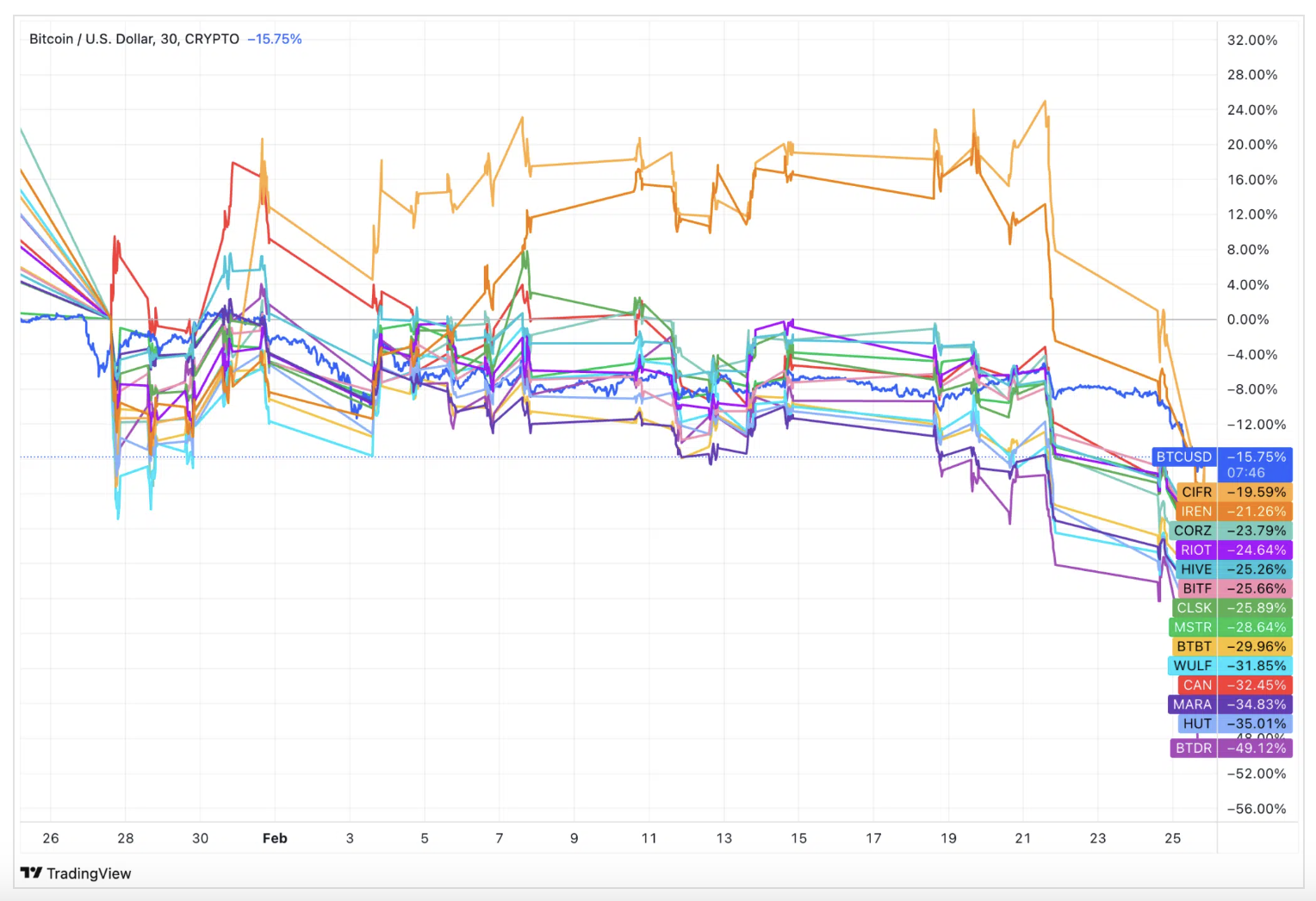

- Bitcoin stays range bound: The past week has been one of the most volatile periods for bitcoin since it broke above $100,000 last December. Bitcoin opened last week at $95,000 before tumbling to a local low of $78,000 on Thursday. Over the weekend, bitcoin snapped back to $94,000 following the Trump administration’s comments on a Strategic Crypto Reserve. At the time of publication, bitcoin's made a round trip back to $86,000.

- Trump reiterates strategic bitcoin reserve promise, adds other coins to the mix: President Trump took to Truth Social over the weekend to reaffirm his administration’s commitment to establish a strategic bitcoin reserve, but he added other cryptocurrencies to the mix. He said that his administration’s digital asset council is "moving forward on a Crypto Strategic Reserve that includes XRP, SOL, and ADA” as well as BTC and ETH. It’s unclear what method the administration would use to establish such a reserve.

Interesting Reads and Videos

- Can Trump Order a Strategic Bitcoin Reserve?

- THE BITCOIN SHAKEOUT w/ Checkmate

- What’s Driving Bitcoin Adoption in 2025?

Bitcoin Mining Market News and Trends

- AI dominates Core Scientific, Riot earnings calls: Core Scientific and Riot reported their 2024 earnings last week, and AI was a central focus of each company’s investor calls.

- For its part, Core Scientific indicated that it’s aiming to diversify its future AI/HPC revenue to the point where its current partner Core Weave would constitute under 50% of this revenue. Since Core Weave is entitled to all of the AI data center capacity that Core scientific is currently developing, to accomplish this, Core would need to retrofit existing bitcoin mining data centers or acquire new centers (as we covered last week, Core Scientific recently leased a 16 MW Alabama data center with intent to purchase). Even with this commitment to diversify its AI clients, Core Scientific also recently announced that it is expanding its contract with Core Weave to an additional 70 MW worth a projected $1.2 billion, bringing the total contract to 590 MW and a projected $10.2 billion over 12 years.

- Riot, which currently has no active HPC/AI business line, signalled further intent to convert its 600 MW phase 2 build out for its Corsicana facility into an HPC/AI data center. Ostensibly with this conversion in mind, Riot has revised its hashrate guidance for 2025 down from 46.7 EH/s to 38.4 EH/s. CEO Jason Les also mentioned that they would potentially evaluate a retrofit of the full 1GW Corsicana facility and its Rockdale facility “if the opportunity was there” and if “the economics made sense.”

- February sell-off shaves $13 billion from public bitcoin miner values: 15 of the leading public bitcoin miners lost $13 billion in their collective market caps over February, according to The Miner Mag. Bitdeer led losses after decreasing 55% over the month, and the collective market caps of the 15 stocks fell from $36.6 billion to $23.2 billion from January 24 to February 25.

Market Overview

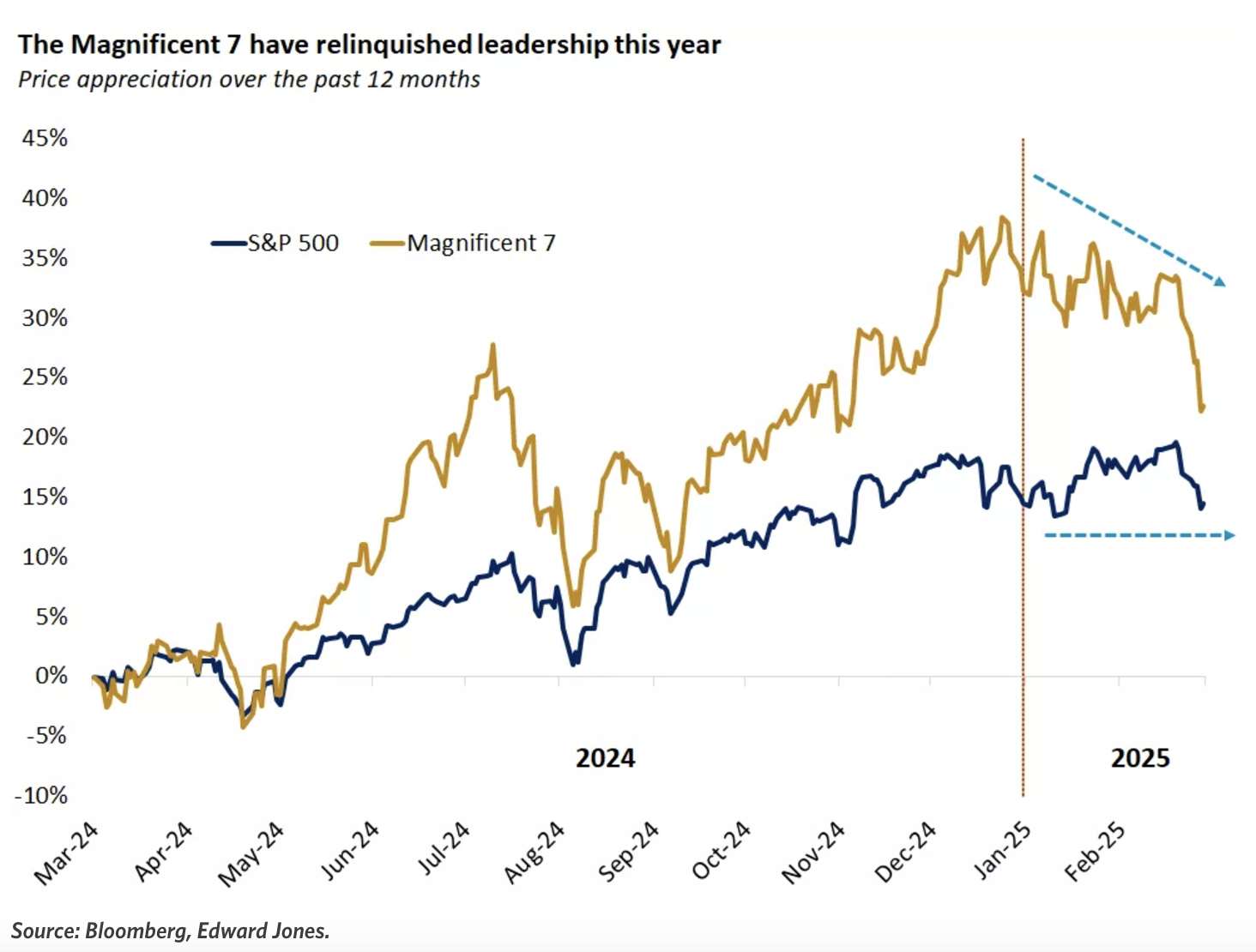

- Equities take a pummeling that scrubbed year-to-date gains: Equities were routed last week, and despite a price pop before market close on Friday, the major indices ended the week in the red with the exception of the Dow. The declines wiped out 2025’s gains for the Nasdaq and Russell 2000 and nearly did so for the S&P 500 as well. The Nasdaq took the biggest hit of the bunch, underscoring a point we highlighted in last week’s letter that the Magnificent 7 and tech stocks in general are leading the market selloff.

- S&P 500: 5,954.50 (-1.20% WoW) | (+1.46% YTD)

- Dow: 43,840.91 (+0.8%) | (+3.42%)

- Nasdaq: 18,847.28 (-3.80%) | (-2.25%)

- Russell 2000: 2,163.07 (-1.71%) | (-3.07%)

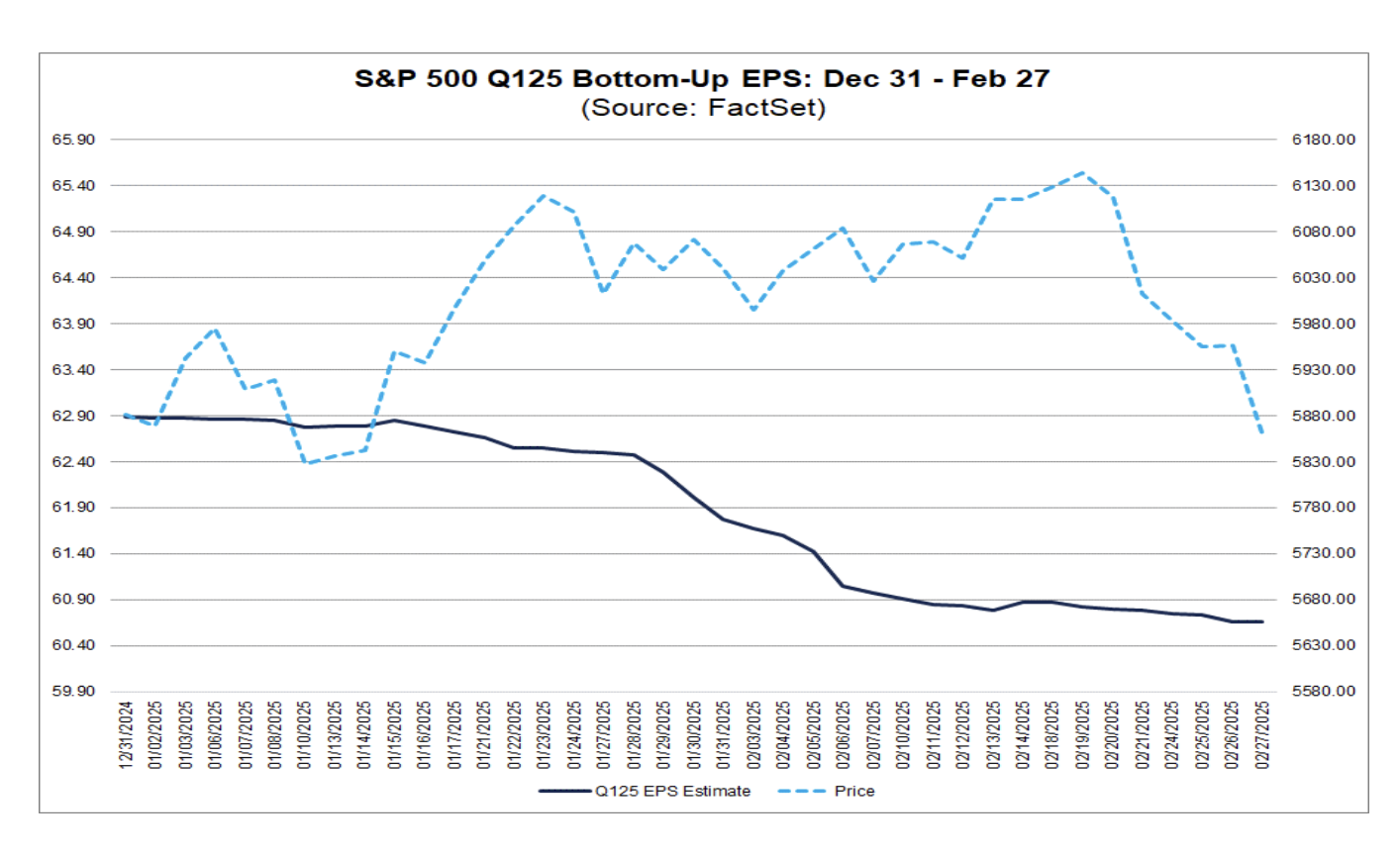

- S&P 500 Q4 earnings scorecard comes in strong: Last week’s market score card might belie a weak Q4 earnings season, but the data show otherwise. Per FactSet, with 97% of Q4 earnings in, 75% of S&P 500 companies reported a positive earnings per share (EPS). FactSet reports that the blended year-over-year growth for the S&P 500 is 18.4% versus December's 11.7% estimate; this was the largest YoY growth since Q4 2021. On the flip side, however, and speaking to the fears that sparked last week’s selloff, 58 S&P 500 companies are projecting negative EPS for Q1, versus 40 issuing guidance for positive EPS.

- A grab bag of fears is shaking markets: A number of anxieties are weighing on the market, from inflation, to consumer confidence, to policy uncertainty, to renewed tariff fears:

- Tariffs are back on the table as the Trump administration stated that tariffs on Canada, China, and Mexico would take effect by March 4. He also signalled intent to levy tariffs against the European Union on April 2.

- Inflation has been sticky, with the U.S. Bureau of Economic Analysis reporting a 2.5% YoY (and 0.3% MoM) increase to headline PCE in January. Meanwhile, The Conference Board’s Consumer Confidence Index plummeted 7 points in February to 98.3; this was the largest drop since August 2021 and brought the index down to its lowest point since June 2024.

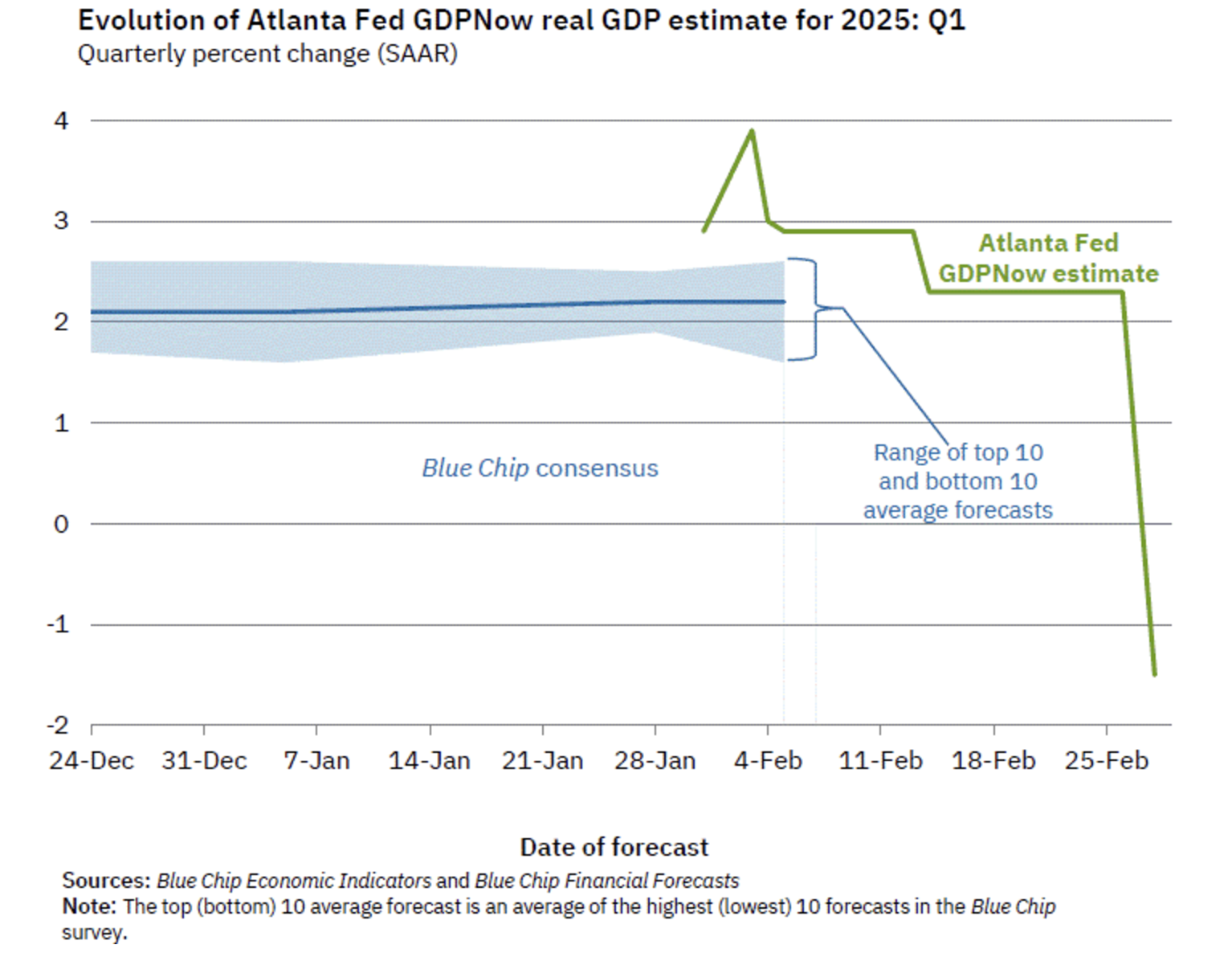

- Atlanta Fed revises Q1 2025 GDP to -1.5%: Following the latest reports from the Bureau of Economic Analysis and U.S. Census Bureau, the Atlanta Fed revised its Q1 2025 GDP forecast down to -1.5% from 2.3%. The revised forecast is informed partly by the U.S. trade deficit widening from $122 billion in December 2024 to $155 billion, and accordingly, the Atlanta Fed is now forecasting -3.7% for contribution of net exports to real GDP for Q1 versus -0.41% in prior estimates. Additionally, consumer spending fell 0.2% in January (versus expectations of a 0.1% rise). Inclement weather across the U.S. may be to blame for the reduction in consumer spending in addition to broader macro uncertainty.

- Oil rises by a hair while natural gas falls:

- U.S. oil prices were essentially flat last week. WTI Crude closed at $70.24/barrel, a 0.1% increase.

- As of the EIA’s Wednesday update, the April 2025 NYMEX contract for the Henry Hub fell $0.25 to $3.96/MMBtu as extreme winter weather across the U.S. calms and melts into Spring.

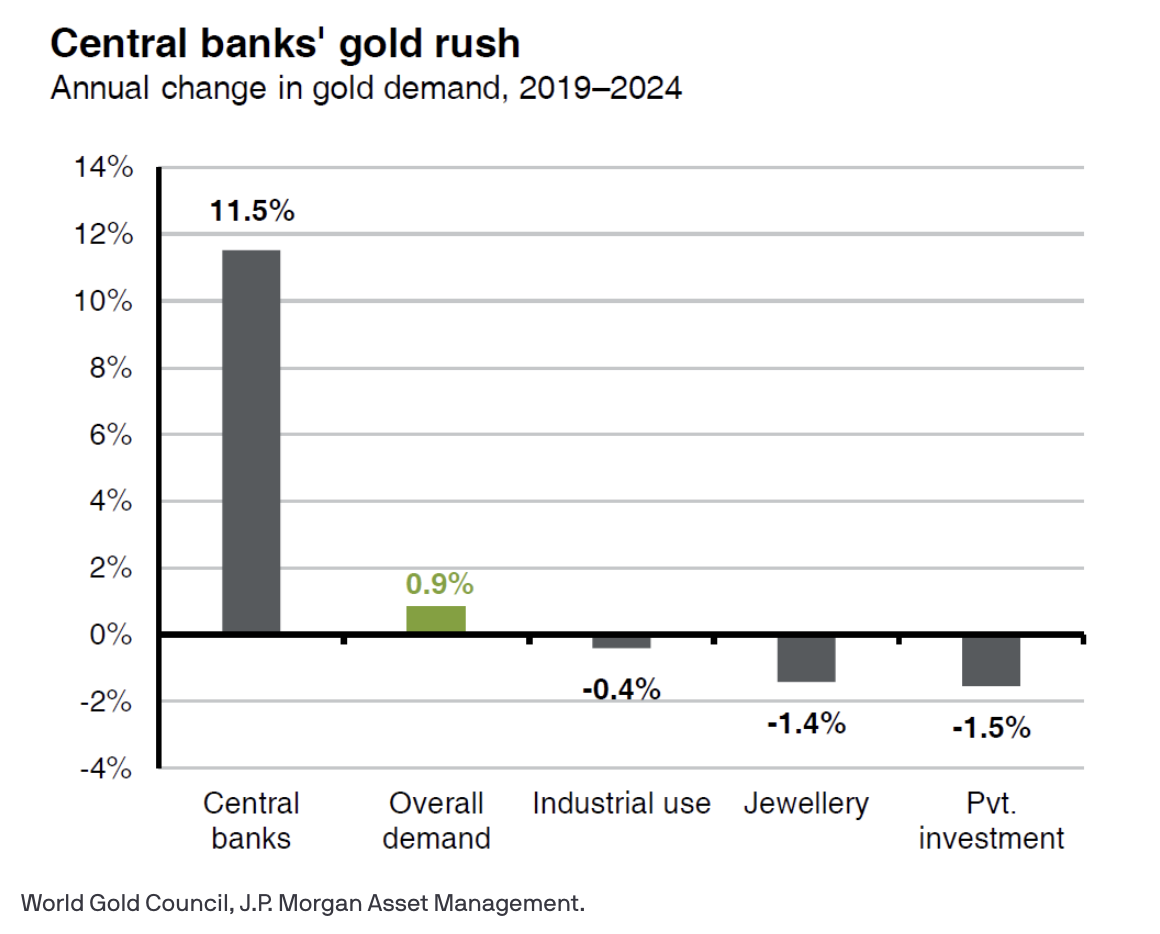

- Central banks were behind gold’s rally to all-time highs: As the macro economy shudders with uncertainty, gold has been setting record highs in 2025, most recently hitting an all-time high of ~$2,950/oz in February. Central banks are behind most of the buying, according to World Gold Council data presented by J.P. Morgan. Since 2019, Central bank annual gold demand has grown 11.5%.

- As economic indicators flash warning signs, Treasury yields fall: Treasury yields have continued their 2025 retreat amid general market turbulence. The yield curve between 10-Year and 3-Month treasuries inverted last week, with the 10-Year falling to 4.20% by week’s end and the 3-Month ending at 4.31%.

- 10-Year: 4.20% (-0.18% WoW) | (-0.38% YTD)

- 5-Year: 4.01% (-0.12%) | (-0.37%)

- 2-Year: 3.99% (-0.10%) | (-0.26%)

The week ahead in data:

- U.S. Census Bureau construction spending report (Monday)

- Institute for Supply Management manufacturing index (Monday)

- ADP National Employment Report (Wednesday)

- Institute for Supply Management non manufacturing index (Wednesday)

- U.S. Census Bureau factory orders report (Wednesday)

- U.S. Census Bureau trade balance report (Thursday)

- U.S. Bureau of Labor Statistic productivity and labor costs report (Thursday)

- U.S. Census Bureau wholesale inventories (Thursday)

- U.S. Department of Labor weekly unemployment claims (Thursday)

- U.S. Bureau of Economic Analysis International Trade in Goods and Services (Thursday)

- U.S. Department of Labor February jobs and unemployment (Friday)

- Federal Reserve consumer credit report (Friday)

Notable corporate earnings this week:

- Okta (Monday)

- GitLab (Monday)

- Target (Tuesday)

- Best Buy (Tuesday)

- Sea Limited (Tuesday)

- MongoDB (Wednesday)

- Marvell Technology (Wednesday)

- Costco (Thursday)

- Broadcom (Thursday)

- JD.com (Thursday)

- Hewlett Packard (Thursday)

Thank you for reading, and please feel free to reach out with any questions.

Christian Lopez